Blog

Freddie Mac Posts Positive Income Numbers, Requests Small Draw

Freddie Mac announced that it has postedrna net income of $619 million for the quarter ended December 31, 2011 and totalrncomprehensive income of $1.5 billion. Inrnthe third quarter the company posted $(4.4) billion as both a net and arncomprehensive loss. For the entire year ofrn2011 Freddie Mac had net income of $(5.3) billion and comprehensive income of $(1.2)rnbillion compared to $(14.0) billion and $0.3 in 2010.</p

The shift from a net loss to a net gainrnin the fourth quarter reflects lower derivative losses due to a smaller declinernin long-term interest rates and a decrease in the provision for credit lossesrnon single-family loans. The shift inrncomprehensive income primarily reflects the net income for the fourth quarter butrnalso the tightening mortgage spreads on some non-agency AFS securities.</p

The company had a net worth deficit ofrn$146 million at the end of the quarter and will submit a request to thernTreasury Department for a draw in that amount. rnThis will be more than offset by a quarterly dividend payment of $1.7rnbillion to Treasury on its holdings of Freddie Mac Senior Preferred Stock. With this draw Freddie Mac will have receivedrn$7.6 billion from Treasury for 2011 and paid $6.5 billion in dividends. In 2010 its draw requests totaled $13.0rnbillion and dividends were $5.7 billion. rnSince being placed in conservatorship in August 2008 Freddie Mac hasrndrawn $72.3 billion from Treasury and paid dividends of $16.5 billion.</p

During 2011 Freddie Mac financedrn$1,859,072 residential properties of which 320,753 were multi-familyrnunits. This was down from 2,115,302rnmortgages in 2010 including 233,952 multi-family units. Total volume in 2011 was $361 billion andrn$412 billion in 2010. The company alsornpurchased 1,183,304 refinance mortgages in 2011 for a total volume of $247rnbillion.</p

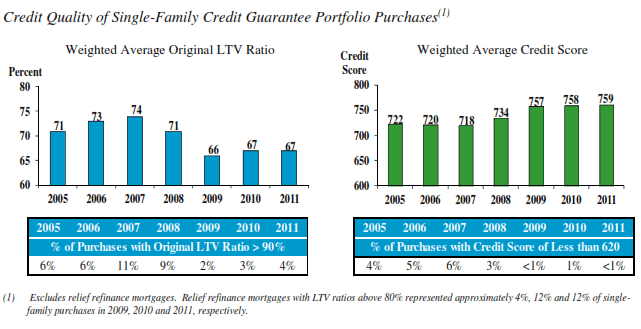

The company said that the loans it acquiredrnafter 2008 continue to perform well and during 2011 represented only 1 percentrnof credit losses while loans originated between 2005 and 2008 represent 90rnpercent of those losses. The currentrndelinquency rate for the newer vintage loans is 0.30 percent compared to 8.75rnpercent for those with 2005-2008 originations. rnThe recent loans were underwritten using more stringent standards andrnhave significantly higher loan-to-value ratios and higher credit scores. These loans now represent more than 50rnpercent of the company’s single-family credit guarantee portfolio.</p

</p

</p

Serious delinquencies were at a rate ofrn3.58 percent at the end of December which the company said was substantiallyrnbelow industry benchmarks. Freddie Macrncontinues to participate in numerous foreclosure prevention activitiesrnincluding representation at hundreds of workshops nationwide and expanding itsrnfree counseling for distressed homeowners in hard-hit cities. The company’s direct activities during 2011rnand (2010) included: 109,174 loan modifications (170,277), 33,421 repaymentrnplans (31,210), 19,516 forbearance agreements (34,594), and 46,163 short sales/deeds-in-lieurnactions (39,175) for a total of 208,274 (275,256) single-family loan workouts.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment