Blog

HAMP: Improved Conversion Rate Helps Boost Permanent Loan Mods in March

Metricsrnfor the Making Home Affordable Program (HAMP) improved substantially duringrnMarch according to data released late Wednesday by the TreasuryrnDepartment. The foreclosure prevention program,rna joint effort by Treasury and the Department of Housing and Urban Development,rnhas been widely criticized for its effectiveness in moving distressed borrowersrninto permanent loan modifications.

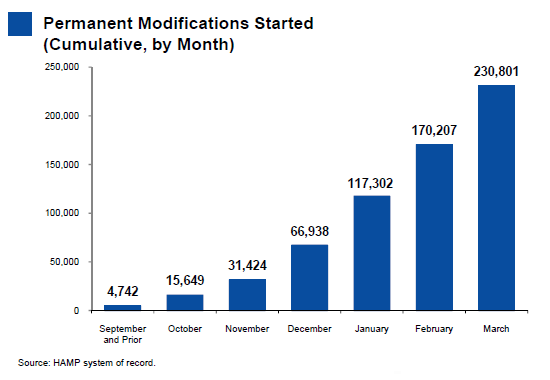

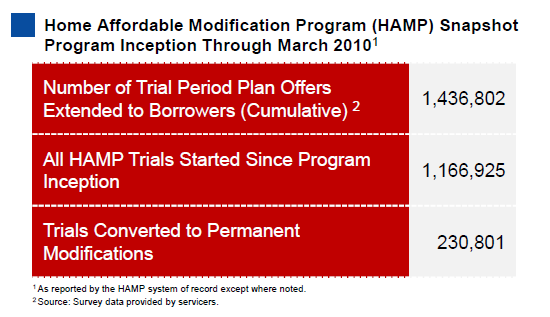

Duringrnthe March, however, over 60,000 homeowners enrolled in the three month trialrnperiod required by the program were converted into permanent modifications. This brings the cumulative total of permanent loan modifcations to 230,801. The Marchrnconversions represent a 15 percent increase over the 53,000 accomplished inrnFebruary and a 3.5-fold rise in permanent modifications sincernthe first of the year. An additional 108,000 permanent modifications arernpending; most are awaiting approval from the borrower.

In terms of the overall conversion rate, 16.1 percent of all offers extended have been converted to permanent loan modifications. Much improved from last month's rate of 12.6 percent. When measuring performance against the number of HAMP trial offers that have actually been accepted, 19.8 percent of homeowners who have completed the 3-month period have been converted to a permanent modification. Again, much better than the 15.6 percent conversion rate reported in February.

Thernnumber of homeowners entering the program, however, is declining as mightrnreasonably be expected after the initial flood of applicants. There were 57,000 new entrants into thernprogram in March compared to 72,000 in February. A total of 1.44 offers for modifications havernbeen extended to borrowers and 1.17 million homeowners have started the trialrnmodification program.

There wasrna large number of trial modifications cancelled during the month. Since the program started in the spring ofrn2009, there have been a total of 155,000 cancellations, 66,500 of which werernrecorded in March. The report providedrnno explanation for this number. A totalrnof 2,879 permanent modifications have been cancelled compared to 1,400 reportedrnlast month.

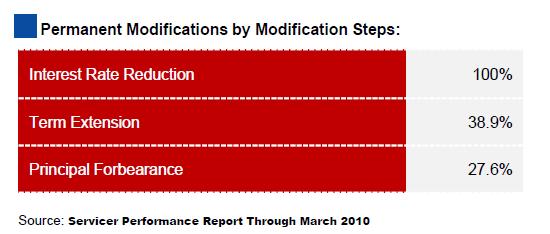

UnderrnHAMP, borrowers are offered a five year modification of their existing mortgagernbased on a debt to income ratio that cannot exceed 31 percent. The servicers who administer the program canrnoffer an extension of the loan term, a reduced interest rate, and/or arnreduction of the principal balance. 100 percent of the modifications to date havernincluded an interest rate reduction, 39 percent have involved an extension ofrnthe term of the loan and 28 percent have had some type of principal reductionrnor forbearance. Servicers have been reluctant to offer forbearance to borrowers and HAMP has recently announcedrna new component of the program to encourage this method of modification.

The HAMPrnreport estimates that approximately 6 million residential mortgages arerncurrently 60 days or more in arrears and that approximately 1.7 million ofrnthese are eligible for the HAMP program. Servicers are encouraged to contact borrowersrnto request information regardless of their apparent eligibility. To date servicers have sent out over fourrnmillion solicitation letters.

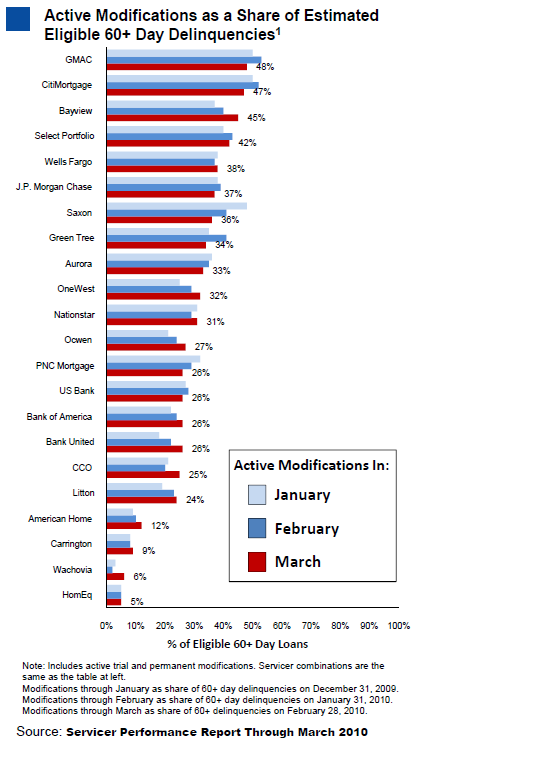

CitiMortgagernand GMAC continue to be the most active participants in the program;both havernnearly 50 percent of their estimated eligible borrowers enrolled intrial orrnpermanent modifications.

Thernreasons for delinquency as reported by the borrowers have remained relativelyrnconsistent over the life of the program; 59.1 percent report that theirrnhardship was caused by a loss of income (a slight increase from 57.4 percent inrnFebruary), 10.5 say it is excessive obligations and 2.8 percent report theirrndelinquency was principally caused by the illness of the principal borrower. Combined with the fact that 44.1rn percent of the 6.5 million unemployed Americans have been out of workfor longer than six months, this statistic implies the truetest of HAMP's success will bewhether or not permanent loan modifications are able to avoidre-default.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment