Blog

LPS Data Shows Long Delays in Foreclosure Process

The specter of shadow inventory looming in the backgroundrnof the housing crisis may be even worse than anticipated according to data releasedrnMonday by Lender Processing Services (LPS). </p

The February Mortgage Monitor report indicatesrnthat, while delinquencies continue to decline, there is an enormous backlog ofrnforeclosures in the pipeline that may be as great as 30 times the monthly salesrnvolume of already foreclosed homes. This implies foreclosed homes will continue to come on the market for many years into the future, continuing downward pressure on home prices in the hardest hit areas thanks to an abundance of vacant and often deteriorating housing units. </p

While there have been occasional spikes over the last year, thernFebruary Mortgage Monitor report shows that both delinquencies and foreclosuresrnstarts have declined steadily over the last year. Foreclosure starts in March 2010 numberedrn250,174; there were 204,916 starts in February 2011 (a decrease of 0.2 percentrnfrom January) and the delinquency rate over the same 12 month period hasrndeclined from 9.66 percent to 8.80 (down 1.2 percent from January.) However the backlog of foreclosures in thernpipeline has continued to expand. Therernare 6.86 million mortgages in some state of delinquency or foreclosurernnationwide, an 8.80 percent delinquency rate, and 2.17 million of those loansrnare 90+ days delinquent and 2.2 million are in foreclosure. In March 2010 there were 7.3 millionrndelinquent mortgages with 2.87 million 90 days or more delinquent and 1.99rnmillion in foreclosure. </p

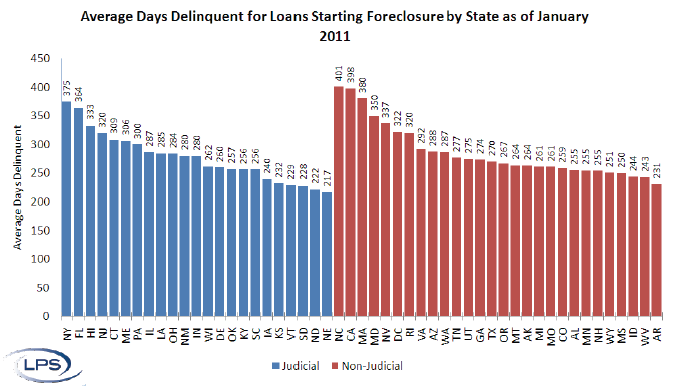

A major reason for the backlog is the steadily increasingrnamount of time loans are spending in the foreclosure pipeline. The average time a loan in the 90+ day bucketrnhas been delinquent by February was 351 days and those in foreclosure had beenrndelinquent for 537 days. In January 2011rnthose figures were 344 and 523 respectively and 12 months earlier, in Marchrn2010, the figures were 278 and 426 days. A full 30 percent of loans inrnforeclosure have not made a payment in over two years. </p

</p

</p

The protracted process as well as lenders’ modificationrnefforts may be working to the benefit of some borrowers as the data shows thatrn22 percent of loans that were 90+ days delinquent 12 months ago are nowrncurrent. There has also been improvementrnin the roll-rate, the numbers of loans that progress from one stage ofrndelinquency to another such as 30+ days to 60+ days. The roll-rate across all stages is now at arnthree year low.</p<pDelinquencies and foreclosures are highest in Florida,rnNevada, Mississippi, New Jersey, and Georgia while the healthiest states inrnterms of their residential mortgage status are Montana, Wyoming, Alaska, SouthrnDakota, and North Dakota.</p

Since the beginning of the foreclosure epidemic there hasrnbeen a subtext of concern over what might happen when the hundreds of thousandsrnof Option ARM mortgages reset. Manyrnexperts worried that resets, when the interest rate, often set even lower thanrnthe prevailing rate when the loan was written, converted to the potentiallyrnmuch higher rate specified in the loan documents, it would trigger a whole newrnwave of delinquent loans and, eventually, foreclosures. This was potentially a more serious problemrnwith Option mortgages than with other adjustable rate loans as the optionrnpayment feature often resulted in negative amortization and thus a largerrnprincipal balance at reset than when the loan originated. According to the Monitor, these Optionrnmortgages are now having significant problems. rn</p

The February data shows that the rate of Option ARMrnforeclosures has increased 23 percent over the last six months and now standsrnat 18.8 percent. LPS says that this is arnhigher level than Subprime foreclosures ever reached. The current delinquency rate for these loansrnis 23 percent. There has also been deteriorationrnin the Non-Agency Prime segment. Both Jumbo and Conforming Non-Agency Primernloans showed increases in foreclosures and were the only product areas withrnincreases in delinquencies.</p

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment