Blog

Natural Disasters are now Measurable Default Risks

Growingrnnumbers of severe weather events throughout the U.S. may be giving new meaningrnto “location, location, location” in the housing world. CoreLogic senior economist Kathryn Dobbynrnwrites in the company’s blog “housing Pulse” that the $8 billion in propertyrndamage caused by severe weather in the U.S. in 2013 is causing the housingrnindustry to think about the risk of any given location’s exposure to naturalrndisasters which are only expected torncontinue to increase in both frequency and intensity.</p

In some parts of the country, suchrnas Florida’s hurricane prone Atlantic coast or the Mid-West’s “Tornado Alley”rnthe risk of unexpected property damage is always there and the mortgagernindustry has relied on required insurance to mitigate its risks. But for a variety of reasons, costs, a lackrnof understanding of the risks, or the absence of a requirement to insurernagainst most specific risks (floods being the exception), many homeowners don’trnmaintain adequate coverage, especially for less common or widely knownrnrisks. Disasters like Hurricane Sandy havernhighlighted this but until recently very little could be done to quantify differencesrnin the risk of a natural disaster from one property to the next.</p

Dobbyn says it is now possible howeverrnto pinpoint these risks at the individual property level, thus helping to protectrnthe homeowner and reduce or prevent losses by the mortgage lender. While she is clearly promoting a new CoreLogicrnservice with her article, the concept and the technology behind it arerninteresting enough to overlook the salesmanship. </p

She says that recent advances inrnspatial and natural hazard sciences make it possible for example to measure wildfirernrisk based on the topography and type of ground cover around a home or tornpredict the likelihood of a property flooding during a hurricane based on thernseverity of the storm. From this sciencernher company has developed a property-specific natural Hazard Risk Score (HRS)rnthat reflects the overall risk of any one disaster or a weighted score forrnseveral natural hazards occurring at the same location. </p

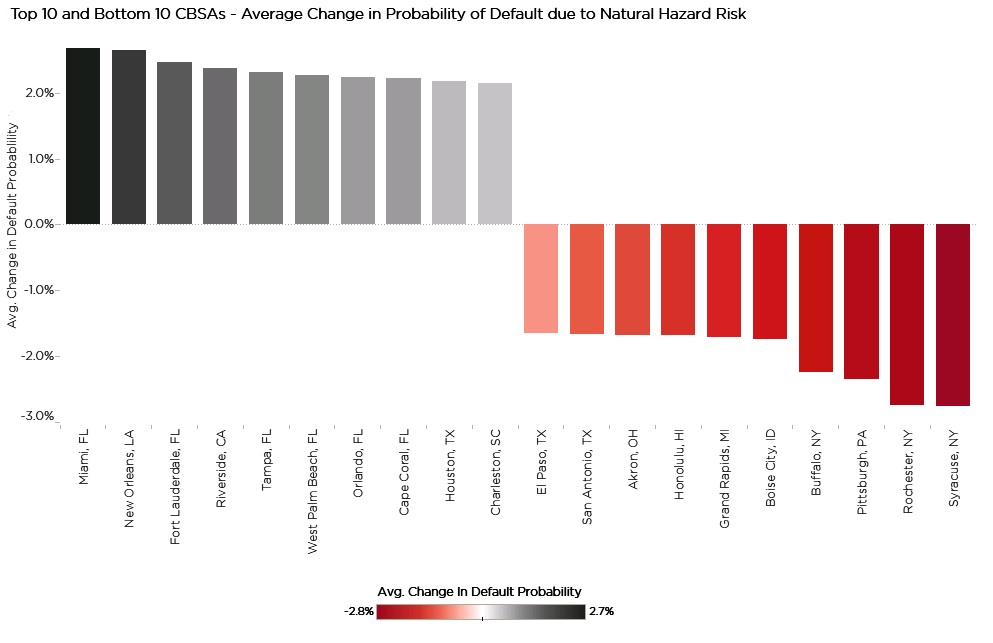

From this what she calls more accuraternprediction of the possibility a mortgage will default based on standardrnmeasures of mortgage default risk (e.g., creditworthiness, ability to pay, loanrnterms and down payment) CoreLogic has estimated a default model that adds inrnthe risk of natural hazards. The companyrnused a random sample of more than 3 million first-lien loans that were activernat some point between January 1995 and March 2014, including prime, subprimernand government loans and were able to measure the reduction and the increase inrnthe average probability of default for markets with a natural hazard risks lessrnthan and greater than the national average hazard risk. </p

</p

</p

It found that seven of the riskiestrnten markets are in Florida with its multiple hazards including wildfires, stormrnsurges, flooding and even sinkholes. The safest markets are in a variety ofrnlocations, but non-coastal New York State had three of the five safest. The typical increase or decrease to accountrnfor natural hazard risk is about 2 to 3 percent, which Dobbyn says is “certainlyrnnot inconsequential when one considers that mortgage default rates, recentrnhistory excepted, are very low to begin with.”</p

As long as Americans continue torngrow in numbers and continue to like living along the coasts the housing stockrnwill be increasingly susceptible to natural disasters and now CoreLogicrnmaintains that mortgage risk can be assessed by a property’s specific locationrnand its propensity for natural disasters.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment