Blog

OCC Notes Higher Delinquencies but Increasing Modification Successes

The eight national banks and single federalrnsavings association servicing the largest loan portfolios reported that firstrnmortgage performance declined across all categories of delinquencies during thernsecond quarter of 2011. The informationrnis part of the Office of Comptroller of the Currency (OCC) Mortgage MetricsrnReport released on Thursday which covers 63 percent of all outstanding firstrnmortgages in the nation.</p

According to the report, current andrnperforming loans represented 88.6 percent of the banks’ portfolios in the firstrnquarter but declined to 88 percent by the end of the second quarter. This is still an improvement from the secondrnquarter of 2010 when 87.3 percent of the loans in the portfolios were current.</p

</p

</p

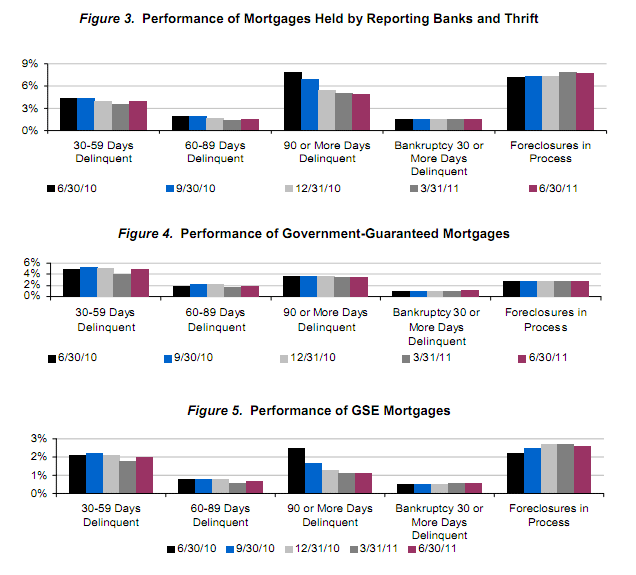

Similar to the overallrnportfolio of mortgages, the performance of mortgages held by reporting banksrnand thrift declined in the second quarter of 2011 to an 80.3 percent ratio ofrncurrent and performing loans, down from 80.4 percent the previous quarter butrnup from 77.2 percent a year ago. Thernpercentage of performing government guaranteed mortgages decreased to 85.7rnpercent from 87.0 percent in Q1 but was improved from 85.3 one year ago. FreddiernMac and Fannie Mae mortgages perform better than the overall portfolio becausernof a higher percentage of prime loans. rnCurrent and performing loans constituted 93.1 percent at the end of Q2rncompared to 93.2 percent at the end of Q1 and 92 percent in Q1 2010. </p

</p

</p

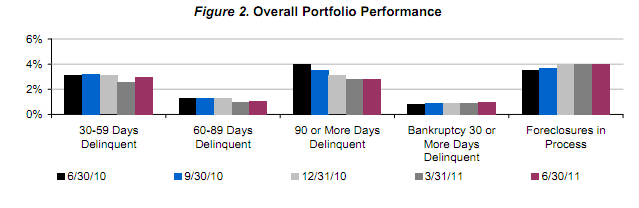

Early stage delinquencies, i.e. mortgagesrnthat are 30 to 59 days delinquent, increased from 2.6 percent of the portfoliornin the first quarter to 3 percent, reflecting seasonal effects in addition tornthe sluggish economy and elevated unemployment. rnSeriously delinquent mortgages – those over 60 days delinquent andrndelinquent mortgages held by bankrupt borrowers, increased one basis point torn4.9 percent of the portfolio, ending five straight quarters when this categoryrntrended down. Both early stage andrnserious delinquencies were down from a year earlier by .9 percent and 19.9rnpercent respectively. </p

The percentage of mortgages in thernprocess of foreclosure was unchanged at 4 percent of the total portfolio andrnwhile completed foreclosures increased 1.2 percent quarter-over-quarter, thernnumbers were down more than 30 percent from the second quarter of 2010. While the yearly decrease was significant,rnOCC warned that completed foreclosures may continue to increase in futurernquarters as a large number of delinquent loans work through the process and borrowersrnexhaust other alternatives. </p

Short sales increased by 12.6rnpercent during the second quarter and now represent 31 percent of all homernforfeiture actions. Deeds-in-lieurnincreased by almost 50 percent but still represent less than 1 percent of homernforfeitures.</p

Servicers implemented 456,397 homernretention actions during the quarter, nearly twice the 287,145 new foreclosurernproceedings. Most of these actions werernunder the Home Affordable Modification Program (HAMP) which increased by 31.6rnpercent during the quarter while other actions were down. The net result was a decrease of 18.1 percentrnin new retention actions compared to the first quarter. Servicers have modifiedrn2,083,464 mortgage loans from the beginning of 2008 through the end of thernfirst quarter of 2011.</p

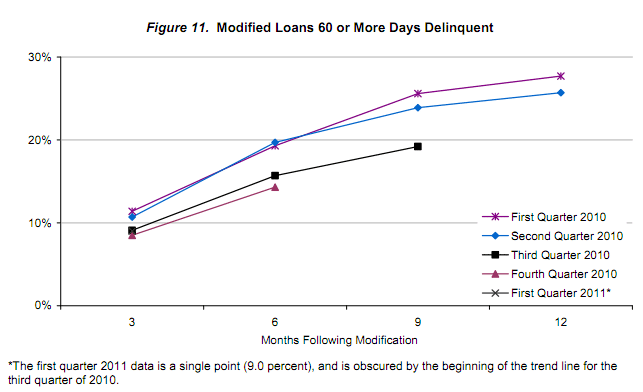

There has been increasing successrnwith these modification efforts. rnMortgages modified in recent quarters have improved steadily overrnearlier modifications and have performed consistently better than has beenrnhistorically the case for such loans. Atrnthe end of the second quarter of 2011, 51.3 percent of modifications remainedrncurrent or had been paid off. Another 9.2 percent were 30-to-59 daysrndelinquent, and 18.2 percent were seriously delinquent. More than 10rnpercent were in the process of foreclosure and 5.3 percent had completedrnthe foreclosure process. Of the 938,180 modifications implemented duringrn2010, 62.4 percent were current or paid off. Another 10.4 percent werern30-to-59 days delinquent, 15.2 percent were seriously delinquent, and 8.4rnpercent were in the process of foreclosure or had completed the foreclosurernprocess. The table below shows thernsteadily improving performance metrics of modified loans over the last fivernquarters.</p

</p

</p

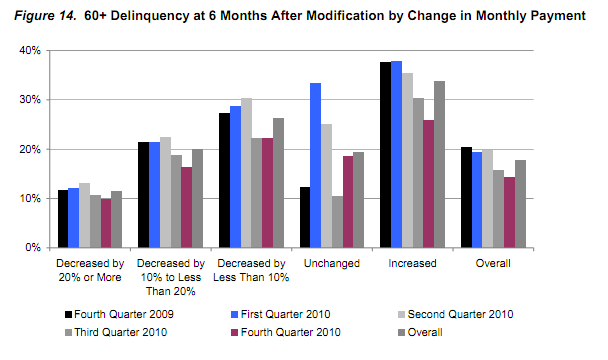

The on-going emphasis on sustainingrnthe modifications by lowering the monthly payment is apparently paying off inrnreduced defaults. As the figure belowrnshows, as the amount of the payment reduction increases, the default raternconsistently goes down. </p

</p

</p

Modifications done under HAMP arernperforming much better than those done under other auspices. A chart comparing the performance of HAMPrnmodifications with other modifications done in the last five quarters at threernmonth intervals results in 14 cohorts. rnHAMP modifications significantly outperformed other modifications in allrnbut the three month data point for loans modified in Q4 2010. That deficiency was overcome three monthsrnlater. </p

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment