Blog

RealtyTrac: Foreclosure Discount Higher, Short Sales Jump

RealtyTrac,rnthe Irvine California firm that reports on all things foreclosure said onrnThursday that, while sales of bank-owned real estate and homes in some stage ofrnforeclosure during the second quarter of 2011 was mixed in comparison withrnearlier quarters, the gap in sales price between distressed and market raternsales continued to widen. </p

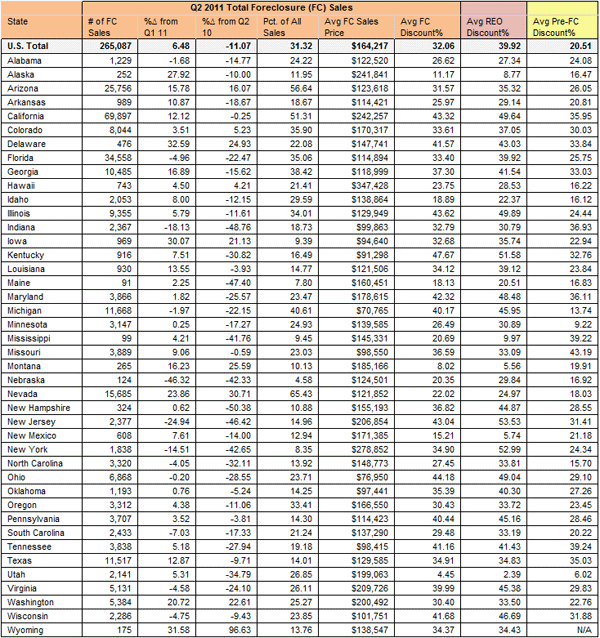

Salesrnof properties that were either sold out of bank inventories (REO), at auction,rnor while in some stage of default through a short or other sale increased 6rnpercent over revised first quarter sales to a total of 265,087 propertiesrnnationwide. This was a decrease of 11rnpercent from the number sold one year earlier. rnThe market share of distressed homes dropped from 36 percent of allrnsales in the first quarter but was up from 24 percent one year earlier.</p

Thernaverage sales price of distressed homes was $164,217 in the second quarter,rndown less than 1 percent from the first quarter and five percent from one yearrnearlier. On average distressed homesrnsold for 32 percent less than a home that was not in foreclosure compared to arn27 percent discount in Quarter One.</p

“With average prices on disrtessed real estate trending down and average discounts trending up, thisrnreport is clearly good news for well-positioned buyers and investors lookingrnfor bargain real estate that will build them wealth in the long term and oftenrncash flow as rental real estate in the short term,” said James Saccacio chiefrnexecutive officer of RealtyTrac. “Maybe less evident, however, is the good newsrnin this report for distressed homeowners looking to sell, and even lendersrnsaddled with large portfolios of delinquent loans.</p

Thernreport illustrates some significant differences between homes sold while theyrnare in the process of foreclosure – i.e. in default or scheduled for auction -rnand those in bank inventory. First ofrnall, pre-foreclosure sales were up sharply, increasing 19 percent from thernfirst quarter to 102,407 properties while REO sales were stalled at 162,680rntransactions, only about 200 fewer than in the first quarter. Year-over-year pre-foreclosure sales wererndown 12 percent and REO sales declined 10 percent. Pre-foreclosure sales accounted for 12rnpercent of all real estate sales in the second quarter, unchanged from Q1 andrnup from 10 percent one year earlier. REOrnsales had a 19 percent market share in the second quarter compared to 23rnpercent in the first quarter and 15 percent in Q2 of 2010</p

Pre-foreclosures,rnwhich are often sold via short sale where the bank agrees to a smaller payoffrnthan the actual loan balance, had an average sales price nationwide ofrn$192,129, a discount of 21 percent below the average sales price ofrnnon-foreclosure homes. That discount was up from a 17 percent discount in thernprevious quarter and a 14 percent discount in the second quarter of 2010. REOsrnhad an average sale price of $145,211, nearly 40 percent below the averagernmarket price. This is an increase fromrnthe 36 percent discount that was the average in Q1 and a 34 percent discountrnone year earlier.</p

Pre-foreclosuresrnsold in the second quarter took an average of 245 days to sell after receivingrnthe initial foreclosure notice, down from an average of 256 days in the firstrnquarter – following three straight quarters of increases in the average time tornsell pre-foreclosures. REOs took anrnaverage of 178 days to sell after being foreclosed, an increase of two daysrnsince the previous quarter and 14 days more than in the second quarter ofrn2010. This REO marketing time, however,rnis on top of the time it took the bank to foreclosure and take possession ofrnthe property.</p

Saccaciornsaid, “The jump in pre-foreclosure sales volume coupled with biggerrndiscounts on pre-foreclosures and a shorter average time to sellrnpre-foreclosures all point to a housing market that is starting to focus onrnmore efficiently clearing distressed inventory through more streamlined shortrnsales – at least in some areas. Thisrngives distressed homeowners who do not qualify for loan modification orrnrefinancing – or who are not interested in those options and want to sell – arnbetter chance of completing a short sale to avoid foreclosure. Streamlinedrnshort sales also give lenders the opportunity to more pre-emptively purgernnon-performing loans from their portfolios and avoid the long, costly andrnincreasingly messy process of foreclosure and the subsequent sale of an REO -rnwhich may end up selling for a lower price than it would have as arnpre-foreclosure short sale and in the meantime further stresses alreadyrnoverloaded REO departments.”</p

</p

</p

Foreclosure-relatedrnsales accounted for 65 percent of all residential sales in Nevada during thernsecond quarter, the highest percentage of any state. Third parties purchased arntotal of 15,685 homes in foreclosure or bank owned during the second quarter,rnup 24 percent from the first quarter and up 31 percent from the second quarterrnof 2010. The average discount in Nevadarnwas just over 22 percent. </p

InrnArizona distressed property sales accounted for 57 percent of sales at arndiscount of 27 percent. In Californiarnthe market share jumped to 57 percent, a 12 percent increase over in Q1,rnreturning the state to the same level as one year earlier. </p

Thernstates with the largest price differential between market and foreclosure salesrnwere Kentucky (48 percent) and Ohio (44 percent). California, Illinois, and New Jersey allrnreported discounts over 43 percent. Twornstates, Montana and Utah, reported average discounts in the single digits. Utah, which is consistently among the statesrnwith the highest level of foreclosure activity, reported a discount of 4.5rnpercent and 2.39 percent for properties sold from REO. RealtyTrac does not offer any explanationrnfor this anomaly.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment