Blog

Study: No Additional Restrictions on QRM Needed

The proposed down payment standardsrnfor new mortgages might push 60 percent of potential borrowers into high-costrnloans or out of the housing market altogether according to a paper releasedrntoday by the Center for Responsible Lending. The paper,<iBalancing Risk and Access: UnderwritingrnStandards for Qualified Residential Mortgages, is the result of a study tornweigh the effects of proposed underwriting guidelines for qualified residentialrnmortgages (QRM), mortgages that are exempt from the risk retention requirementsrnlaid out in the Dodd-Frank Wall Street Reform Act. </p

The Center, a nonprofit, nonpartisanrnresearch and policy organization with a stated mission of “protectingrnhomeownership and family wealth by working to eliminate abusive financialrnpractices” has, along with other consumer and industry groups, raised concernsrnabout a potential disproportionate impact of restrictive QRM guidelines onrnlow-income, low-wealth, minority and other households traditionally underservedrnby the mainstream mortgage market. Thernstudy examines the way different QRM guidelines may affect access to mortgagerncredit and loan performance and estimates the additional impacts on defaultsrnresulting from guidelines above and beyond QM product requirements. </p

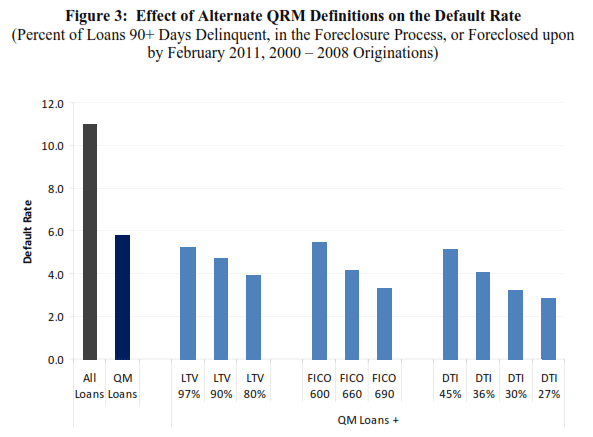

The researchers, Roberto G. Quercia,rnUniversity of North Carolina Center for Community Capital, Lei Ding, WaynernState University, and Carolina Reid, Center for Responsible Lending usedrndatasets from Lender Processing Services (collected from servicers) andrnBlackbox (data from loans in private label securities collected from investorrnpools.) They identified from among 19rnmillion loans originated between 2000 and 2008 the 10.9 million that would meetrnthe current QRM guidelines, i.e. loans with full documentation that have nornnegative amortization, interest only, balloon, or prepayment penalties. Adjustable rate mortgages must have fixedrnterms of at least five years and no loans over 30 years duration. </p

The default rate for the universe ofrnloans was 11 percent, for prime conventional loans, 7.7 percent, and for loansrn(regardless of type) that would have met the QM product feature limits, 5.8rnpercent. In other words, the research “suggestsrnthat the QM loan term restrictions on their own would curtail the risky lendingrnthat occurred during the subprime boom and lead to substantially lowerrnforeclosure rates without overly restricting access to credit.”</p

The next step was to apply some ofrnthe suggested additional criteria for QRM to the loans; a minimum down paymentrnof 20 percent, a range of higher FICO scores, and lower debt to income (DTI)rnratios. The goal was to determine thernbenefit of each as measured by an improvement in default rates without an undo reductionrnin borrowers able to qualify for an affordable loan.</p

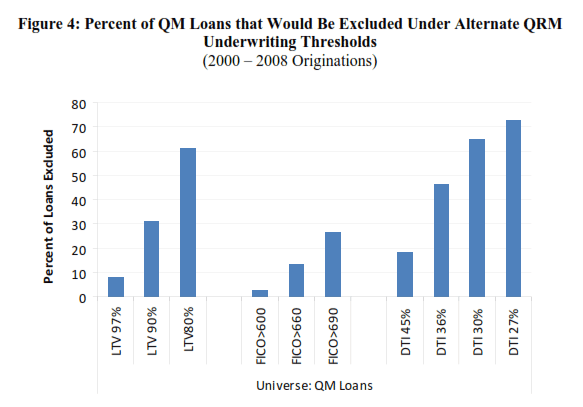

When various permutations ofrnloan-to-value (LTV), FICO scores, and DTI ratios were applied to the loans lowerrndefault rates were achieved. Thesernimprovements, however, were accompanied by the exclusion of a larger share ofrnloans. As Figure 4 shows, some of the restrictionsrnresulted in the exclusion of as many as 70 percent of loans. </p

</p

</p

</p

</p

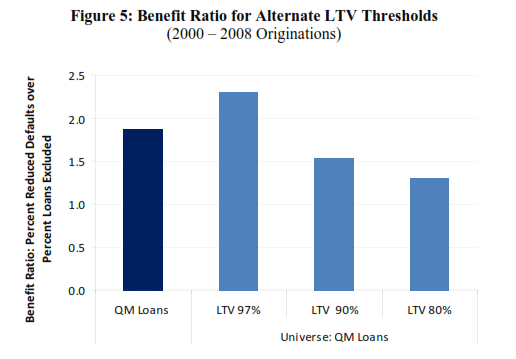

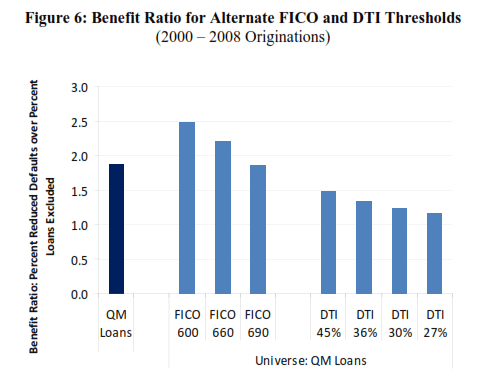

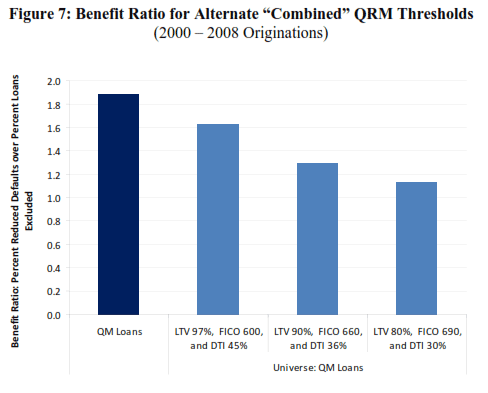

To quantify this, the authorsrndeveloped two additional measures. Thernfirst, a benefit ratio, compares the percent reduction in the number ofrndefaults to the percent reduction in the number of borrowers who would havernaccess to QRM loans with the proposed guidelines. For example, an underwriting restriction thatrnresulted in a 50 percent reduction in foreclosures while excluding only 10rnpercent of borrowers would have a higher benefit ratio than one with the samernreduction in foreclosures that excluded 20 percent of borrowers.</p

</p

</p

One finding was that LTVs of 80 orrn90 percent resulted in particularly poor outcomes while an LTV of 97 percentrnhad added benefits of reduced defaults relative to borrower access. This suggests that even a very modest down paymentrnmay play an important role in protecting against default while excluding arnsmaller share of borrowers than would a higher down payment requirement.</p

Since underwriting is unlikely tornimpose restrictions in isolation, the study analyzed a combination of possiblernQRM restrictions. They found that thernstrictest guidelines produced the worst outcomes and that none of the patternsrnof proposed restrictions performed as well as the QM restrictions on their own.</p

</p

</p

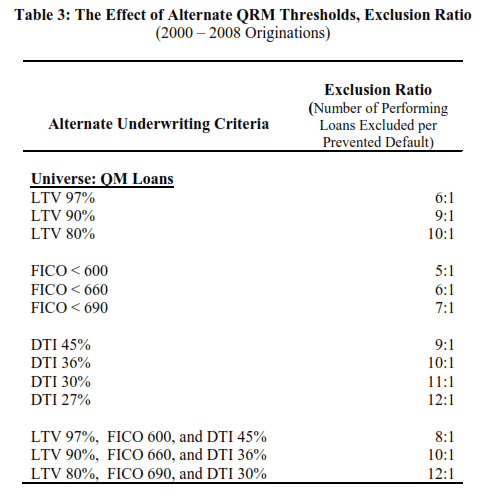

The second measure, an exclusionrnratio, looks at the number of performing loans a certain threshold wouldrnexclude to prevent one default. In thisrnmeasure, the number of excluded loans can be viewed as a proxy for the numberrnof “creditworthy” borrowers who would be excluded from the QRM market. </p

</p

</p

Imposing 80 percent LTV requirementsrnon the universe of QM loans would exclude 10 loans from the QRM market tornprevent one additional default. Addingrnto this a FICO above 690 and 30 percent DTI ratio would exclude 12 creditworthyrnborrowers to prevent one default.</p

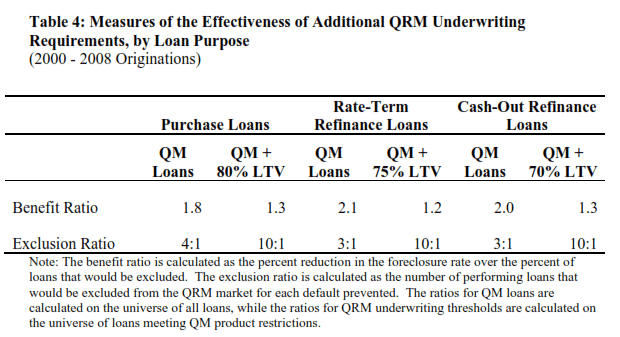

The current QRM criteria are morernrestrictive for rate-term and cash-out refinancing than for purchasernloans. The study found that the QMrnproduct restrictions are the most effective in balancing the demand between reducingrndefaults and ensuring access to credit.</p

</p

</p

The study also found that imposingrnadditional LTV, DTI, and FICO underwriting requirements on QM loans hadrndisproportionate effects on low-income borrowers and borrowers of color. Just over 75 percent of African-Americanrnborrowers and 70 percent of Latino borrowers would not qualify for a 20 percentrndown QRM mortgage and significant racial and ethnic disparities are evident forrnFICO requirements as well. At FICOrnscores above 690, 42 percent of African-Americans and 32 percent of Latinornborrowers would be excluded against 22 percent of white and 25 percent of Asianrnhouseholds. At the most restrictiverncombined thresholds (80 percent LTV, FICO above 690, DTI of 30 percent) approximatelyrn85 percent of creditworthy borrowers would not qualify with African Americanrnand Latino disqualifications each above 90 percent.</p

The Center says in conclusion thatrnits research provides “compelling evidence that the QM product loan guidelinesrnon their own would curtail the risky lending that occurred during the subprimernboom and lead to substantially lower foreclosure rates, while not overlyrnrestricting access to credit.”

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment