Blog

Existing Home Sales Give Back Incentivized Gains. Jobs Still the Main Roadblock

The National Association of Realtors released December Existing Home Sales data this morning.

Whenrnnew homes are being built AND selling, money moves around the economyrnmore efficiently. The size of the housing market combined with thernbroad influences it has over the economy make the real estate sector arnreliable leading indicator of economic activity. Real estate is one ofrnthe first sectors to contract when a recession is looming and one ofrnthe first to show signs of recovery when economic activity begins tornimprove.

BUT…

Whenrnviewing housing data and its influence over the broader economy,rnExisting Home Sales are not as forward looking as other housingrnindicators such as housing starts and building permits. This is for arnfew reasons…

Think about the materials that go into BUILDING arnhome….WOOD, STEEL, PLASTICS, WIRING, PIPING, CONCRETE, GLASS,rnELECTRICITY, FURNITURE, CARPETING, ELECTRONICS, APPLIANCES….LABOR.

Theserngoods and services are not a part of the money transfer process of anrnExisting Home Sale. Existing Homes are already built, and while therernare more and more ” foreclosure fixer uppers” on the market, thernoverall economic activity boost seen from a spike in new constructionrnis absent when discussing the Existing Home Sales supply chain.

Also,rnexisting home sales data is only reported at the time of closing, whenrnthe deed is actually transferred to the new owner. It can take up tornthree months for a purchase transaction to close, if it closes at allrnas the origination process remains cluttered with roadblocks andrndelays. On top of this, the additional tightening of credit guidelinesrnis expected to continue to reduce the number of qualified borrowers whornare looking to buy. With that in mind, while the exhaustion of existingrnhome supply is a key part toward growth in new residentialrnconstruction, Existing Home Sales data is considered less forwardrnlooking than other indicators like building permits and housing starts.

NOVEMBER EXISTING HOME SALES

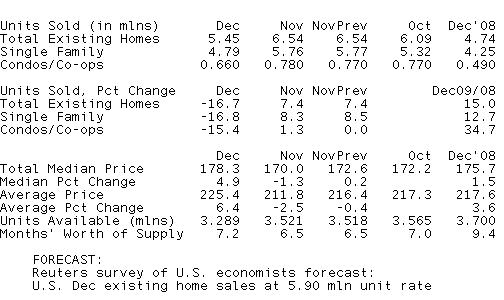

In November, the NAR reported that sales of previously owned homes rose 7.4% to an annual rate of 6.54 million sales.rnSingle family homes led the overall index higher, recording an uptickrnfrom 5.32 million sales to 5.77 million annual sales. Supply ofrnpreviously owned homes fell from 3.565 million to 3.518 million, at therncurrent annual pace of existing home sales, this was 6.5 months ofrnsupply. Raw unsold inventory figures are 15.5 percent below levels onernyear.

DECEMBER EXISTING HOME SALES

Consensus Estimate: 5.90 million annual pace of existing home sales

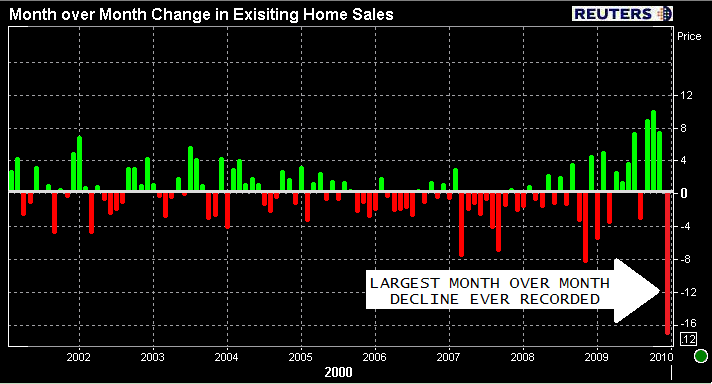

Result: Worse than Expected. -16.7 percent at 5.45 million annual sales

From the NAR…

After a rising surge from September through November, existing-homernsales fell as expected in December after first-time buyers rushed torncomplete sales before the original November deadline for the taxrncredit.

Existing-home sales – including single-family, townhomes, condominiums and co-ops – fell 16.7 percent to a seasonally adjusted annual rate of 5.45 million units in December from 6.54 million in November, but remain 15.0 percent above the 4.74 million-unit level in December 2008.

Herernis the month over month change, this was the worst monthly declinernsince the NAR began reporting on Existing Home Sales in 1968.

Single-family home sales fell 16.8 percent to a seasonally adjustedrnannual rate of 4.79 million in December from a pace of 5.76 million inrnNovember, but are 12.7 percent above the 4.25 million level in Decemberrn2008. For all of 2009, single-family sales rose 5.0 percent torn4,566,000.

Existingrncondominium and co-op sales fell 15.4 percent to a seasonally adjustedrnannual rate of 660,000 in December from 780,000 in November, but arern34.7 percent higher than the 490,000-unit pace a year ago. For all ofrn2009, condo sales rose 4.8 percent to 590,000 units.

Raw unsold inventory is 11.1 percent below a year ago, isrnat the lowest level since March 2006, and is 28.2 percent below thernrecord of 4.58 million in July 2008.

For all of 2009 there were 5,156,000 existing-home sales, which wasrn4.9 percent higher than the 4,913,000 transactions recorded in 2008; itrnwas the first annual sales gain since 2005.

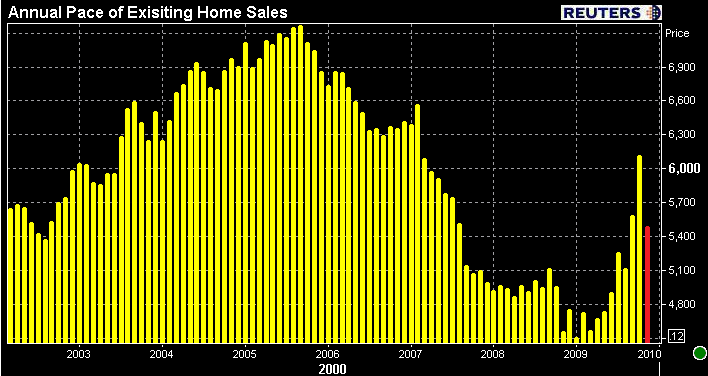

Total housing inventory at the end of December fell 6.6 percent torn3.29 million existing homes available for sale, which represents arn7.2-month supply at the current sales pace, up from a 6.5-month supplyrnin November. Here is the number of existing home sales expected to take place annually at the current pace of demand.

Regionally:

- The Northeast dropped 19.5 percent to an annualrnlevel of 910,000 in December, 21.3 percent above a year ago. Thernmedian price in the Northeast was $241,700, up 3.2 percent fromrnDecember 2008.

- The Midwest fell 25.8rnpercent in December to a level of 1.15 million, 8.5 percentrnhigher than December 2008. The median price in the Midwest wasrn$143,200, which is 1.8 percent above a year ago.

- The South dropped 16.3 percent to an annual pace of 2.01rnmillion in December, 15.5 percent above December 2008. Thernmedian price in the South was $152,000, down 1.0 percent from a yearrnago.

- The West declined 4.8 percent to anrnannual rate of 1.38 million in December but are 15.0 percent higherrnthan a year ago. The median price in the West was $236,000, up 2.7rnpercent from December 2008.

The national median existing-home price for all housing types wasrn$178,300 in December, which is 1.5 percent higher than December 2008.

The median existing single-family home price was $177,500 in December,rnwhich is 1.4 percent above a year ago. For all last year, thernsingle-family median was $173,200, down 11.9 percent from 2008. The medianrnexisting condo price was $183,700 in December, up 1.0 percent fromrnDecember 2008. For all of last year, the median condo price wasrn$176,100, which is 16.1 percent below 2008.

Distressed homes, whichrnaccounted for 32 percent of sales last month, continue to downwardlyrndistort the median price because they generally sell at a discountrnrelative to traditional homes in the same area. For all of 2009, thernmedian price was $173,500, down 12.4 percent from $198,100 in 2008;rndistressed homes accounted for 36 percent of total sales last year.

An NAR practitioner survey shows first-time buyers purchased 43rnpercent of homes in December, down from 51 percent in November. Repeatrnbuyers rose to 42 percent of transactions in December from 37 percentrnin November; the remaining sales were to investors.

Here is a recap of the data:

Here are some quotes of interest from the release…

Lawrence Yun, NAR chief economist:

“It’s significant that home sales remain above year-ago levels, but the market is going through a period of swings driven by the tax credit,”

“We’ll likely have another surge in the spring as home buyers take advantage of the extended and expanded tax credit. By early summer the overall market should benefit from more balanced inventory, and sales are on track to rise again in 2010. However, the job market remains a concern and could dampen the housing recovery – job creation is key to a continued recovery in the second half of the year.”

“The median price rose because of an increased number of mid- to upper-priced homes in the sales mix,”

————————————————————

Going into this report we knew the recent spike in Existing Home Sales was a function of an anticipated expiration of the FTHB tax credit. That said, although the drop was more than anticipated, it was not unexpected that Existing Home Sales would decline in December. They did…no big deal.

Looking ahead, nothing has changed, the same old issues are seen as being roadblocks to expansion in the housing market and macro-economy.

We need to work off current supply of all homes available on the market. In order for that to happen we need qualified buyers and borrowers. Those buyers and borrowers need stable jobs.

The first time home buyer tax credit has been a huge help in this effort, so too has the Fed's MBS Purchase Program. While the extension and expansion of the home buyer tax credit is progressive, from a buyer's perspective I still see several issues that will deter demand.

Failed loan modifications, an uptick in foreclosures, and continually high delinquency rates are the main argument against an evolving positive forward looking outlook. Some like to throw in the notion that shadow inventory will be counterproductive once demand is more stable and home prices find level ground. While there really isn't much we can do about added supply due tornforeclosures (loan mod programs really not doing great), there is a degree of “self policing” the market has overrna voluntary increase in home supply (new construction and shadowrninventory). It's all about perceptions of economic reality.

Last week, builders informed us they are READY AND WILLING to start construction but do not plan to break ground until the labor market is creating jobs. Once home builders see it fit to begin pouring new foundations, the overall economy should be showing significant signs of improvement. If both home builders and prospective home sellers are feeling confident enough to begin building or put their house on the market, it would imply there was enough improvement in the demand side of the equation to justify the move. We have to hope home buildersrnand looming home sellers time their strategies accurately. If builders are too optimistic, they may end up adding unwanted supply of new homes to the still overcrowded marketplace. If there really is an overhang of shadow inventory and it comes to market, a huge spike in supply would add downward pressure to home prices and hurt the overall economic outlook. READ MORE ON THE HOME BUILDING OUTLOOK.

Both events assume the macro-economy is prepared to handle increased supply. This puts us back to the same spot we've been stuck in for months: ALL IS DEPENDENT UPON JOBS

This is where I copy and paste a very familiar message…

Until jobs are being created for the herd of citizens on unemployment benefits, the housing market will likely undergo a slow, frustrating recovery process.

If you dont have a job, find a way to make yourself a more attractive labor source. Technology is replacing human brawn. More and more computers are performing production responsibilities humans once held. Costs are still being cut and operations are being more productive with their resources. While this will eventually lead to more hiring in the future, job creation will be focused on specific intellectual capabilities. Some jobs will be lost forever, human labor must be able to manage new technology.

The point: If you are without a job, dont waste this “time off”. Go back to school. Re-educate and re-tool. Get new certifications and licenses. Find a way to evolve your intellectual capabilities. The labor market will be very competitive for years to come.

Its that “chicken or the egg” dilemma again!

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment