Blog

Existing Home Sales/Prices Slip Despite More First Time Buyers

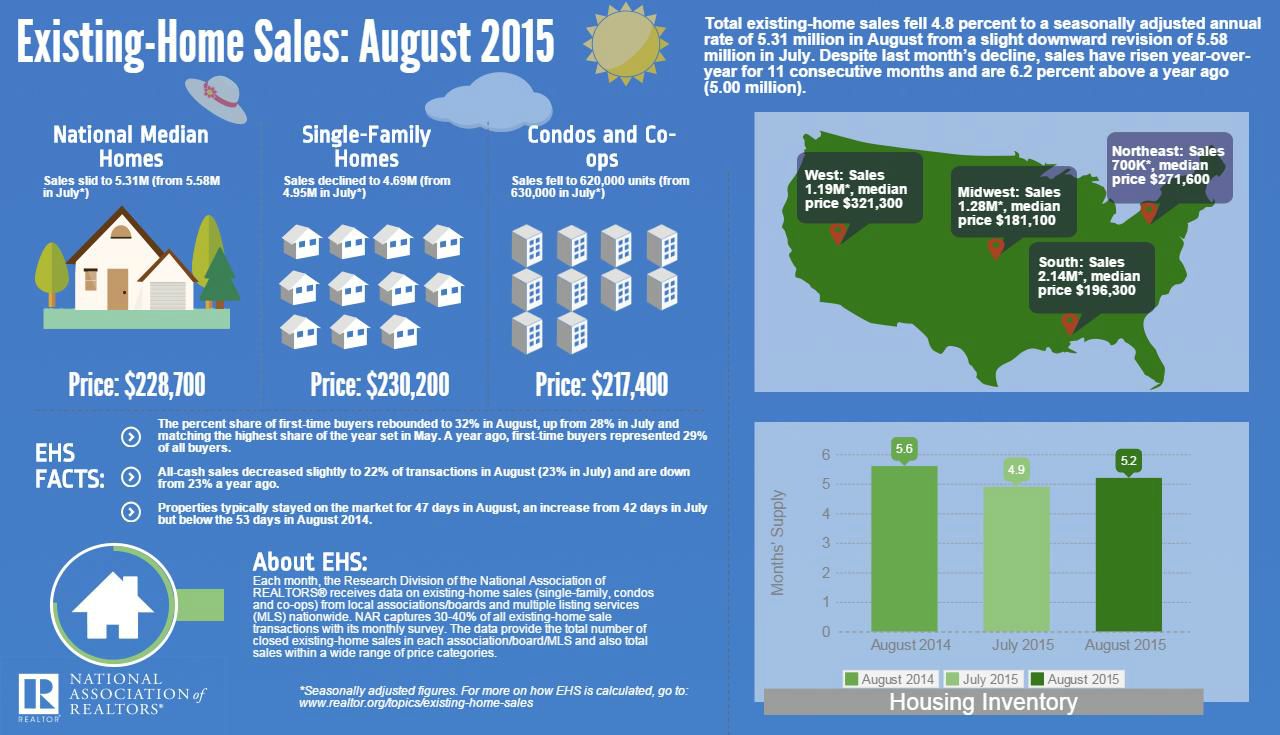

Even as the market share of first-timernbuyers continued to inch up, overall sales of existing homes declined inrnAugust. The National Association ofrnRealtors® (NAR) said today that total existing home sales fell 4.8 percent to arnto a seasonally adjusted annual rate of 5.31 million units in August from arnslight downward revision of 5.58 million in July. The dip came on the heels of three straightrnmonths of increases and despite slowing price growth.</p

</p

</p

Existing home sales are completedrntransactions that include single family homes, townhomes, condominiums, andrnco-ops. While August sales were down,rnNAR notes that sales have now risen year-over-year for 11 consecutive monthsrnwith August 2015 sales registering a 6.2 percent gain from a year earlier whenrnsales were at a 5.0 million rate.</p

Single-family home sales declined 5.3rnpercent to a seasonally adjusted annual rate of 4.69 million in August fromrn4.95 million in July, but remain 6.1 percent higher than the 4.42 million pacerna year earlier. Existing condominium and co-op sales declined 1.6 percent to arnseasonally adjusted annual rate of 620,000 units in August from 630,000 unitsrnin July, still a solid 6.9 percent higher than the 580,000 unit pace in Augustrn2014. </p

Lawrence Yun, NAR chief economist, saysrnhome sales in August lost some momentum to close out the summer. “Salesrnactivity was down in many parts of the country last month – especially in thernSouth and West – as the persistent summer theme of tight inventory levelsrnlikely deterred some buyers,” he said. “The good news for the housingrnmarket is that price appreciation the last two months has started to moderaternfrom the unhealthier rate of growth seen earlier this year.”</p

The median price for all existing housingrntypes was $228,700, representing annual appreciation of 4.7 percent from thernmedian of $218,400 in August 2014. The increasernwas the 42nd consecutive year-over-year gain. The median existingrnsingle-family home price rose 5.1 percent from last year to $230,200 and the medianrnexisting condo price was up 2.2 percent to $217,400. </p

Existing home inventories gained a bitrnof ground; rising 1.3 percent to 2.29 million homes, a 5.2 month supplyrncompared to 4.9 months in July. Therncurrent inventory is 1.7 percent lower than in August 2014.</p

“With sales and overall demandrnhigher than a year ago and supply mostly unchanged, low inventories will likelyrncontinue to limit options for those looking to buy this fall even with thernoverall pool of buyers shrinking because of seasonal factors,” adds Yun.</p

The percent share of first-time buyers</brebounded to 32 percent in August, up from 28 percent in July and matching thernhighest share of the year set in May. A year ago, first-time buyers representedrn29 percent of all buyers. Individual investors accounted for 12 percent of existingrnhome sales in August, 1 percentage point lower than in July. All cash sales decreased from a 23 percentrnshare of sales in July to 22 percent in August. Sixty percent of investors paidrncash in August.</p

Distressed sales, foreclosures andrnshort sales, remained at a 7 percent in August for the second month, matchingrnthe lowest share since NAR began tracking in October 2008, Five percent ofrnsales were foreclosures that sold at an average discount of 18 percent below marketrnvalue and 2 percent were short sales, averaging discounts of 12 percent</p

Yun says when the Federal Reservernfinally decides to left short-term interest rates he doesn’t expect arnpronounced impact on mortgage rates or overall housing demand. “With job growth holding steady,rnprospective buyers can handle any gradual rise in mortgage rates – especiallyrnif today’s stronger labor market finally leads to a boost in wages andrnhomebuilding accelerates to alleviate supply shortages and slow price growth inrnsome markets,” he said.</p

Properties typically stayed on thernmarket for 47 days in August, an increase from 42 days in July but below the 53rndays in August 2014. Short sales were on the market the longest at a median ofrn124 days while foreclosures sold in 66 days and non-distressed homes took 45rndays. Forty percent of homes sold in August were on the market for less than arnmonth.</p

According to a NAR survey of itsrnRealtor members conducted in August, more than 80 percent of respondents indicatedrnthey had taken some sort of training (webinar, class, etc.) to prepare for the<supOctober implementation of the TILA-RESPA Integrated Disclosure rule (TRID).rnNAR President Christ Polychron said “As the ruling goes into effect nextrnmonth, communication is crucial between all parties involved in a real estaterntransaction to ensure consumers get to closing seamlessly and without delay.rnNAR will monitor the progress of the rule in the weeks ahead and will share anyrnconcerns that arise as part of our continued partnership with the ConsumerrnFinancial Protection Bureau.”</p

None of the four major regionsrnexperienced existing home sale increases in August. Sales in the Northeast were at an annual raternof 700,000, unchanged from July and 6.1 percent above a year ago. The medianrnprice in the Northeast was $271,600, annual appreciation of 2.4 percent. </p

In the Midwest sales declined 1.5rnpercent to a rate of 1.28 million but remain 5.8 percent above the previous August.rnThe median price in the Midwest was $181,100, up 4.0 percent from a yearrnearlier.</p

Existing-home sales in the South fellrn6.6 percent to an annual rate of 2.14 million but 5.9 percent above August 2014.rnThe median price in the South was $196,300, up 6.0 percent year-over-year. </p

Sales in the West dropped 7.8 percentrnto an annual rate of 1.19 million 7.2 percent above a year ago. The medianrnprice in the West was $321,300, up 7.1 percent over 12 months.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment