Blog

Fed MBS Program Update: $34 Billion Left to Spend With Four Weeks to Go

The Federal Reserve today reported on their weekly purchases of agency mortgage-backed securities (MBS).

In the week ending March 3, 2010, the Federal Reserve purchased a net total of $10.00 billion agency MBS. This represents a $1 billion decline from the previous reporting period and breaks a three week streak of $11 billion net total purchases.

The goal of the Federal Reserve's agency MBS program is to provide support to mortgage and housing markets and to foster improved conditions in financial markets more generally. Only fixed-rate agency MBS securities guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae are eligible assets for the program. The program includes, but is not limited to, 30-year, 20-year and 15-year securities of these issuers. (NY Fed MBS FAQs)

Since the inception of the program in January 2009, the Fed has spent $1.22 trillion in the agency MBS market, or 97.3 percent of the allocated $1.25 trillion, which is scheduled to run out at the end of this month. With four weeks left in the program there is now only $34.08 billion in funds remaining.

Of the net $10.00 billion purchases made in the week ending March 3, 2010:

- $100 million was used to buy 30 year 4.0 MBS coupons. 1 percent of total weekly purchases

- $6.60 billion was used to buy 30 year 4.5 MBS coupons. 66 percent of total weekly purchases

- $2.30 billion was used to buy 30 year 5.0 MBS coupons. 23 percent of total weekly purchases

- $1.00 billion was used to buy 15 year 4.5 MBS coupons. 10 percent of total weekly purchases

63 percent of the mortgage-backs purchased were Fannie Mae MBS, 36 percent were Freddie Mac coupons, and 10 percent were Ginnie Mae. 90 percent of purchases were 30 year MBS coupons.

The Fed's daily purchase average during the trading week was $2.0 billion per day. This is $200 million less than the previous reporting period daily average of $2.2 billion. If the Fed were to evenly disperse the remaining $34.08 billion over the next 4 weeks, they would average $1.70 billion purchases per day or $8.52 billion per week.

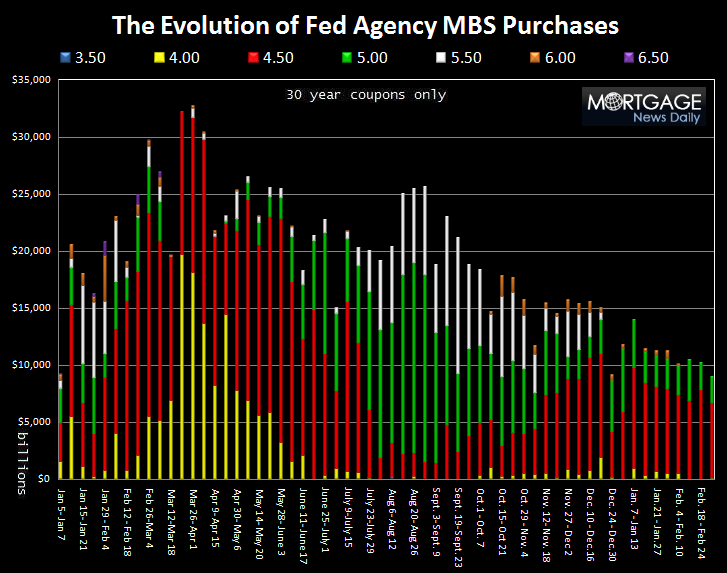

Below is a chart illustrating the evolution of the Federal Reserve's Agency MBS Purchase Program. Notice over the past few months the Fed has reduced their purchases and used remaining funds to offset new loan production supply, 4.50 (RED) and 5.00 (GREEN) MBS coupons specifically, which has helped keep mortgage rates low relative to benchmark Treasury yields.

So far the gradual reduction in the Fed's weekly purchases has been counterbalanced by the slowdown in new loan production. If remaining funds are spread out equally over the next 4 weeks, soon there will not be enough $$$ to offset average new loan production supply from originators (currently running under $2 billion per day). While we do not expect the Fed to exit the program in this manner, we still anticipate that yield spreads will begin to widen against benchmark Treasuries in the next few weeks. This means mortgage rates should start rising compared to Treasuries in the next month.

Currently, the secondary market current coupon (essentially the MBS yield lenders use to derive par mortgage rates after servicing and guarantee fees) is 4.268%. The 10 year Treasury note yield is 3.609%.

Yield Spread Calculation: 4.268% – 3.609% = 66.2 basis points.

When the Federal Reserve does exit the agency MBS market, we estimate the secondary market current coupon yield spread will widen out as high as 100 basis points over 10 year Treasury yields. This would put the MBS yield lenders use to derive par mortgage rates at 4.609%.

If the 10 year Treasury note touches 4.00% and the current coupon yield spread widens to 100 basis points, the MBS yield lenders would use to derive the par mortgage rate would be 5.00%. This is the base yield used to set mortgage rates. If 10 year Treasury yields do touch 4.00% in the months ahead, we expect the average par 30 year fixed mortgage rate to approach 5.50%. We do not expect 10s to break 4.00% in the first half of 2010.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment