Blog

Fed MBS Purchase Program Update: $89 Billion Left to Spend

The Federal Reserve today reported on their weekly purchases of agency mortgage-backed securities (MBS).

In the week ending January 27, 2010, the Federal Reserve purchased a total of $12.50 billion agency MBS. In those five days the Federal Reserve sold $500 million (supported the roll market) for a net total of $12 billion purchases.

The goal of the Federal Reserve's agency MBS program is to provide support to mortgage and housing markets and to foster improved conditions in financial markets more generally. Only fixed-rate agency MBS securities guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae are eligible assets for the program. The program includes, but is not limited to, 30-year, 20-year and 15-year securities of these issuers.

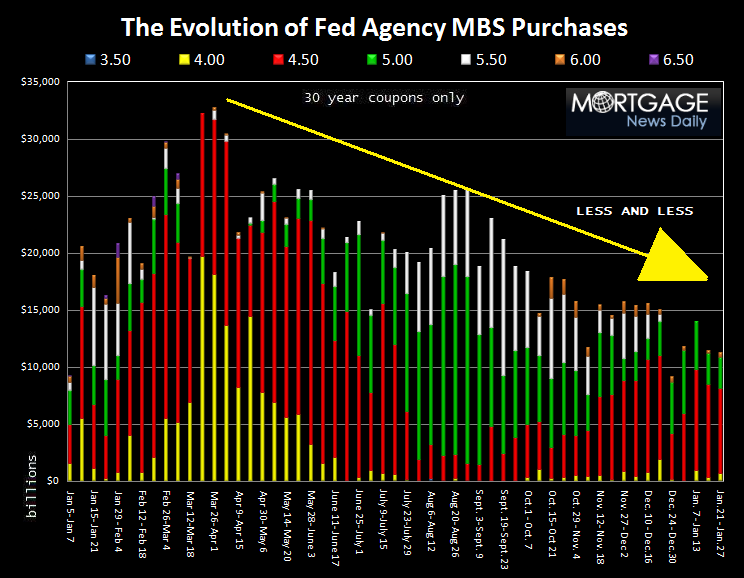

Since the inception of the program in January 2009, the Fed has spent $1.16 trillion in the agency MBS market, or 92.87 percent of the allocated $1.25 trillion, which is scheduled to run out in March 2010. This leaves $89.1 billion left to purchase MBS coupons in the TBA market.

Of the net $12.00 billion purchases made in the week ending January 27, 2010:

- $600 million was used to buy 30 year 4.0 MBS coupons. 5.00 percent of total weekly purchases

- $7.50 billion was used to buy 30 year 4.5 MBS coupons. 62.50 percent of total weekly purchases

- $2.70 billion was used to buy 30 year 5.0 MBS coupons. 22.50 percent of total weekly purchases

- $450 million was used to buy 30 year 6.0 MBS coupons. 3.75 percent of total weekly purchases

- $450 million was used to buy 15 year 4.0 MBS coupons. 3.75 percent of total weekly purchases

- $300 million was used to buy 15 year 4.5 MBS coupons. 2.50 percent of total weekly purchases

35.0 percent of the mortgage-backs purchased were Fannie Mae MBS, 42.5 percent were Freddie Mac coupons, and 22.5 percent were Ginnie Mae. 94 percent of purchases were 30 year MBS coupons.

The Fed's daily purchase average was $2.40 billion per day, a decrease from last week's daily average of $3.00 billion per day. If the Fed were to evenly disperse the remaining $89 billion over the next 9 weeks, they would average $1.98 billion purchases per day or $9.9bn per week.

Given the slowdown in the mortgage market, this should be enough to offset new loan production supply from originators.

Below is a chart illustrating the evolution of the Federal Reserve's Agency MBS Purchase Program. Notice over the past few months the Fed has reduced their purchases and used remaining funds to offset new loan production supply, 4.50 (RED) and 5.00 (GREEN) MBS coupons specifically, which has helped keep mortgage rates low. Overall, weekly purchases continue to decline, yet mortgage valuations remain stable.

I have been exploring the Fed's eventual exit from the MBS purchase program and how it might impact the industry. Michael Fratantoni, MBA's VP of Research and Economics, summed up the mortgage environment PERFECTLY:

“Although rates remain low, there appears to be a smaller pool ofrnborrowers who are willing and able to refinance at today's rates.”

This is why we think the Fed will be able to exit the mortgage marketrnat the end of Q1 2010. Thanks to weakness in the labor market and arnmini-refi boom over the past year, the pool of qualified borrowersrn(refinances and purchases) has shrunk considerably. This impliesrnmortgage loan production will be slow enough to allow the Fed to exitrnthe agency mortgage-backed securities market without causing a majorrndisruption in MBS supply and demand technicals.

WHO WILL PROVIDE DEMAND SIDE SUPPORT IN THE AGENCY MBS MARKET?

Regardless of rich MBS valuations, banks have proven themselves to be arnstable source of demand side MBS support. If/when yield spreadsrn(relative value) cheapen up as the Fed makes their move toward stagernleft, there will be more incentive for hedge funds and money managersrnto become more neutral players (instead of being mostly sellers). Onrntop of these two sources of funding, Asian banks, who usually focus onrnGNMA paper, will likely follow the lead of US banks and maintain orrnincrease their current level of interest in US residential MBS. Therernisn't a better time for the Fed to make an exit…

While much of the direction mortgage rates head is dependent upon the clarity and perception of the macroeconomic outlook (benchmark yields) and the Fed's eventual exit from the MBS market, the fate of the GSEs also plays a role in MBS valuations and mortgage rates.

If the Fed backs out, with delinquencies still sky high and foreclosures showing no sign of slowing, I believe MBS investors will need more than an implied guarantee to provide funding support. Unfortunately, given the Obama Administration's renewed focus on fiscal responsibility, an explicit GSE guarantee seems unlikely, especially when you add in the Christmas eve backstop the Treasury provided to FN/FRE.

Does anyone think the OMB adds the GSEs to the Federal Budget on Monday? Or will a Treasury backstop be enough to keep MBS investor confidence (demand) strong enough to prevent mortgage rates from rising (relative to benchmark yields) ?

Favorable supply/demand technicals are definitly supportive, but I still think investors will want a clearer cash flow guarantee. If nothing new is announced politically, and the Fed still intends to exit the MBS market, expect mortgage rates to rise relative to benchmark yields. I would also expect that the FHA and Ginnie Mae will continue to be relied upon as a liquidity crutch for loan originators looking to sell their mortgages…..

The federal budget, which is expected to be released on Monday, will narrow our options.rn

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment