Blog

Freddie Mac to Eliminate Interest Only Option. Lender Overlays Loom

Freddie Mac is taking another step in the direction of historically responsible lending habits. The Enterprise today announced it would no longer offer interest only loans as of Sept. 2010. Lenders will undoubtedly enforce this guideline change well in advance of the deadline.

HERE is the release:

McLean, VA – Freddie Mac (NYSE: FRE) announced today that on or about September 1, 2010, the company will cease purchasing and securitizing interest only mortgages, including Freddie Mac Initial Interest fixed-rate and adjustable-rate mortgages. Additional information will be provided to Freddie Mac Seller/Servicers in an upcoming Single-Family Seller/Servicer Guide bulletin.

Interest only mortgages, including Freddie Mac Initial Interest mortgages, provide for interest-only payments for a specified period of time beginning with the first monthly payment after the note date, and principal and interest payments on a fully amortizing basis for the remainder of the mortgage term.

Freddie Mac was established by Congress in 1970 to provide liquidity, stability and affordability to the nation's residential mortgage markets. Freddie Mac supports communities across the nation by providing mortgage capital to lenders. Over the years, Freddie Mac has made home possible for one in six homebuyers and more than five million renters.

———————————————————————–

This isn't a huge surprise considering the message currently being sent by the Federal Housing Finance Agency. The central goal of the FHFA in managing its conservatorship of Freddie Mac and Fannie Mae is conserving the assets of the corporations by minimizing their credit losses from delinquent mortgages. Eliminating the interest only option does just that….

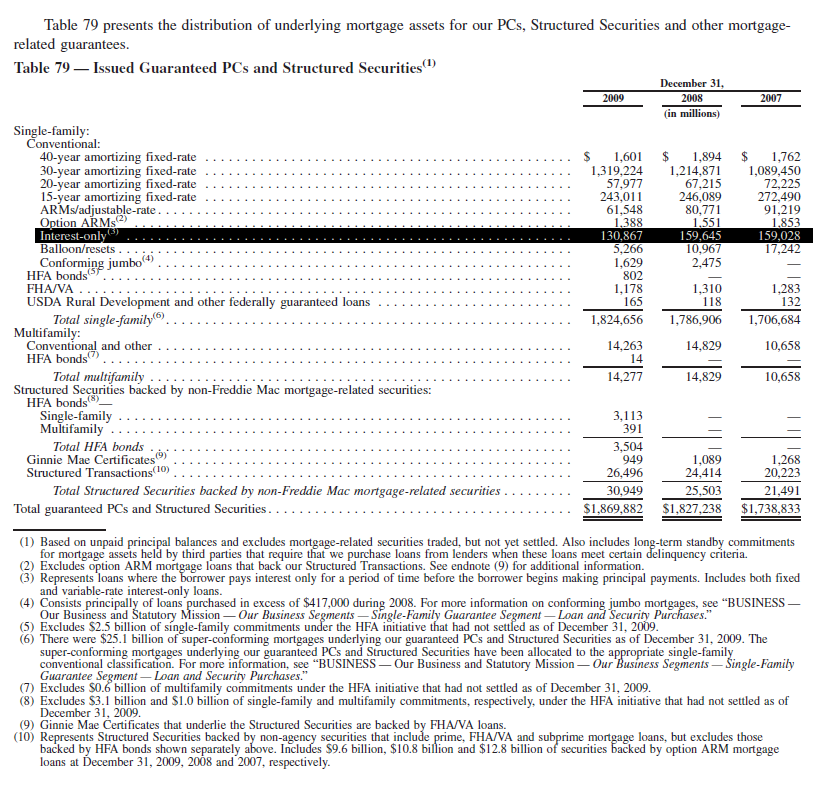

In the 4Q 09 Freddie Mac had guarantees on interest only loans totaling $130.87 billion. This is only 7.2% of their portfolio, down 18% from 2008.

From Freddie's 4Q09 10-K:

“Our single-family mortgage portfolio contained interest-only loans totaling $129.9 billion and $160.6 billion in unpaid principal balance as of December 31, 2009 and 2008, respectively. We purchased $0.8 billion and $23.1 billion of these loans during 2009 and 2008, respectively….These types of loans have experienced higher delinquency rates than other mortgage products. The average FICO score at origination associated with interest-only loans in our single-family mortgage portfolio was 720 at both December 31, 2009 and 2008.”

Plain and Simple: Interest only loans are not performing as well as other loan products. The interest only repayment option is too risky for Freddie and the FHFA.

Based on the credit characteristics of the IO portfolio, its not necessarily unqualified borrowers at the root of this decision. It's a combination of high levels of unemployment and concern over the general health of housing demand and home prices.

More from the 10-k:

“Further declines in U.S. home prices or other adverse changes in the U.S. housing market could negatively impact our business and increase our losses.….We expect that national home prices will continue to decrease in 2010, which could result in a continued increase in delinquencies or defaults and a level of credit-related losses higher than our expectations when our guarantees were issued”

The mortgage finance product offering contraction continues.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment