Blog

Harvard Study Offers New Angle On Bank vs Non-Bank Blame Game

The Harvard Joint Center of Housing Studies recently released a study on the impact of the housing crisis on low-income and minority communities and what can be done to improve their access to mortgage credit going forward. The paper, Getting on the Right Track: Improving Low-Income and Minority Access to Mortgage Credit after the Housing Bust looks at some factors, particularly leading up to the crash, that are not normally brought forward in the seeming endless discussions of the topic, or at least not in quite the same way.

The paper is a comprehensive account of the growth of the housing boom, and interweaves narratives of how seemingly unrelated actions on the part of all market participants were interwoven into what was finally a devastating collapse. The paper is long but worth attention. In this article we will cover what the Joint Center identifies as the causes of the mortgage meltdown and subsequently summarize what the government has done in response, and finally, the Center’s prescription for change.

The homeownership boom that began in the mid-1990s was remarkable for its depth and breadth, but these gains were not evenly shared. Even in the mid-1990s, there was growing concern about the significant gaps between the homeownership rates of racial/ethnic minorities and non- Hispanic whites. Census Bureau figures for 1995 indicated that the homeownership rate was only 42.9 percent among African-American households and 42.0 percent among Hispanic households, nearly 30 percentage points lower than that of non-Hispanic whites. The housing boom did little to change this disparity – the gap in homeownership rates between the minority households and non-Hispanic whites narrowed by about 7 percentage points as policymakers failed to confront the underlying structural factors-growing income inequality and the vestiges of discrimination- perpetuating the gap.

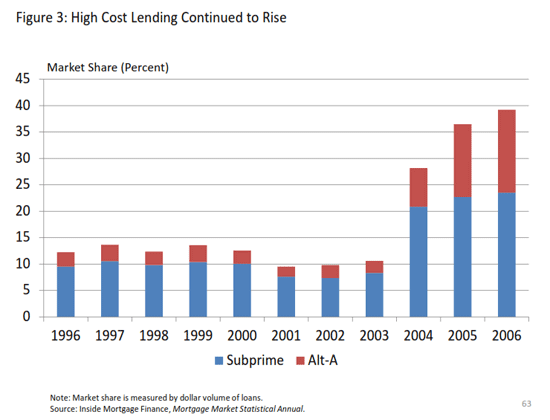

Expansion of homeownership opportunities has been viewed as an important step in reducing inequality in the distribution of income and wealth, but the study says what actually fueled the growth of lower-income and minority lending was a bank/non-bank dual mortgage delivery system. Low income and minority borrowers were targeted by different types of lenders and steered to a different mix of products than commonly found in higher-income markets; products that typically had higher interest rates and less favorable terms than the conventional prime loans available in the mainstream market.

These loans were highly profitable for both primary and secondary market participants, prompting a surge in private label asset-backed securities (PLS) which opened the door to mass securitization of nontraditional mortgage products. Particularly in the case of nonprime residential mortgages, the PLS market suffered from weaker lending standards and more limited counterparty controls and loans were sold to investors that, unless they had capital requirements, did not have to hold any particular level of funds to cover losses.

When house price appreciation slowed and mortgage defaults mounted the collapse of the PLS market triggered a mortgage market meltdown that rocked the world. The resulting constriction of mortgage credit and the mounting wave of foreclosures quickly eliminated the homeownership gains achieved earlier in the decade and bought widespread devastation to the many lower-income and minority communities where subprime lending had been concentrated.

Despite the view of homeownership as the American dream, its direct and indirect contribution to numerous positive outcomes and that it can enable a household to secure decent housing for a relatively low monthly payment, homeownership is not necessarily the best choice for all individuals and families at all times and many households fail to weigh the benefits and costs of ownership. For example, a basic tenet of financial management is that families should diversify their assets; homeownership does the exact opposite by concentrating assets into the purchase of a home while putting the homeowner into a highly leveraged position which could magnify the risk of price declines.

The rapid expansion of homeownership also may have imposed numerous costs on society in general and high costs on racial and ethnic minorities in particular. Families tended to move away from higher-density central city locations to newly growing suburbs, increasing suburbanization and prompting a range of fiscal zoning actions that added to the upward pressure on housing and land costs.

In order to gain access to decent housing, good jobs, and schools these moves took many lower-income and/or minority households to the suburbs or the urban fringe where limited supplies of affordable housing pushed them to buy homes despite the risk. Compounding the problem, unscrupulous mortgage brokers, lenders, and real estate agents preyed upon many low- income, low-wealth borrowers by offering to put them in homes that they could not afford under terms they did not understand.

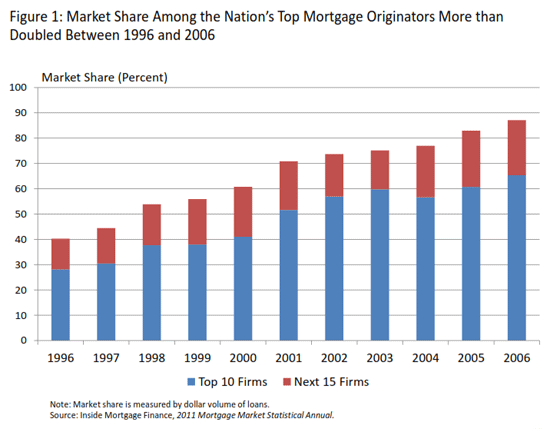

Even as the housing boom was building, advances in computer and telecommunication technology along with the rise of credit scoring and automated underwriting was reshaping the mortgage market. The growing technology required large upfront investments which left many traditional lenders unable to compete. The remaining firms survived by differentiating products, features, and methods of marketing and sales. At the same time origination was decoupled from lending, servicing and securitization, increasing the markets reliance on the government sponsored enterprises (GSEs) and promoting greater specialization to support scale economies and even more concentration. The proliferation of new mortgage products was poorly understood by regulators and consumers; incentives among key players were poorly aligned and abusive practices and outright fraud increased.

The new technology also fostered a switch from the originate-to-hold model to one that originated and distributed through two channels – retail and correspondent and channels, the latter of which typically sold the loans to wholesalers which generally retained servicing rights before selling the loans on the secondary market. These changes which reduced costs also opened the mortgage market to an increasing range of capital sources from within the United States and abroad.

By 2006, the top 25 firms accounted for almost 90 percent of lending-more than double their share a decade earlier and the top 10 originated some 70 percent of loans. Although the larger entities enjoyed reduced costs, they often failed to serve lower-income, higher-risk borrowers who required personal attention and too few were operating in traditionally underserved markets.

The authors point to many of the negative factors in lending that emerged during the housing boom:</p<ul

The various components of the new dual-market mortgage delivery system were governed by an equally complex set of laws and regulations which was slow to adapt to the dramatic changes in the mortgage finance system. Even so, federal regulatory agencies vigorously defended their “turf” and frequently challenged efforts by individual states to oversee abusive lending practices. As a result, many basic consumer protections available in the prime segment of the market were absent or less diligently enforced in the subprime or high-cost segment, and after benefiting little from the homeownership boom, low-income and minority households and communities were especially hard hit during the ensuing bust.

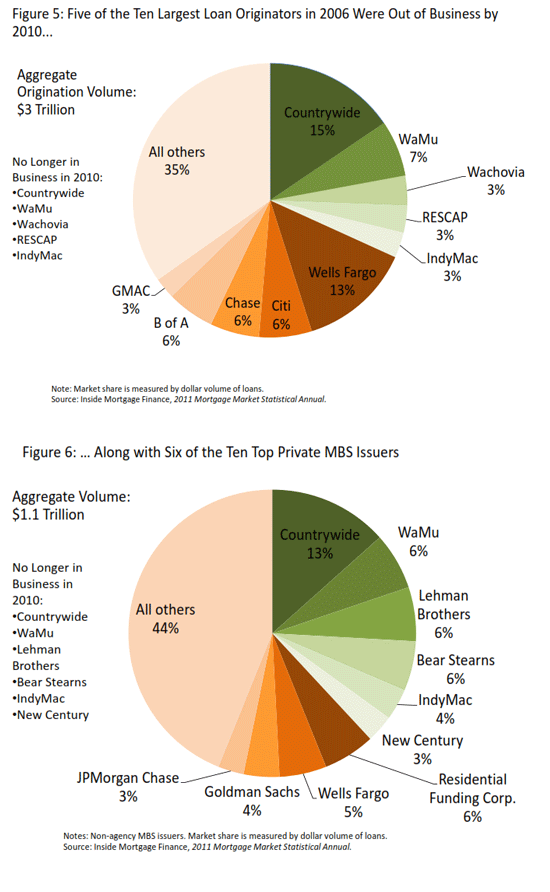

The swift deterioration, especially in subprime loan performance, caught many mortgage lenders and MBS and PLS investors unaware. Early payment defaults shot up in 2006 as more and more borrowers became delinquent within the first six months of their mortgages then in 2007 the decline in the ABX designed to enable investors to trade exposure to the subprime market without holding the actual asset-backed securities, indicated substantially lower investor appetite for securities backed by subprime loans. These events triggered a dramatic loss of confidence in subprime securities. Investors demanded that originating lenders buy back millions of dollars of subprime loans, leading to the unprecedented failure of more than 100 institutions and the splitting up and selling of others. Five of the largest loan originators were out of business by 2010 along with six of the ten top MBA issuers.

FHA, which had lost its traditional market share of low income and minority first time homebuyers to subprime lenders during the boom fared relatively well in the collapse but the GSEs, near failure, were placed in federal conservatorship in August 2008.

With more and more toxic securities blowing up around the world, the U.S. financial system teetered on the brink of collapse and the economy headed into a recession of unknown proportions. Beginning in 2008 and continuing today, the government has introduced numerous initiatives to stabilize the housing and financial markets and to help those hardest hit by the crisis. In a subsequent article we will summarize the Joint Center’s account of these initiatives and their results and look at the broad program which it is proposing going forward.</p

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment