Blog

Lenders Cushion Loan Pricing After Spike in Refinance Demand. Who is Refinancing?

The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending August 13, 2010. </p

The MBA's loan application survey covers over 50% of all U.S. residential mortgage loan applications taken by retail mortgage bankers, commercial banks, and thrifts. The data gives economists a snapshot view of consumer demand for mortgage loans. In a low mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out a lower monthly payment. If consumers are able to reduce their monthly mortgage payment and increase disposable income through refinancing, it can be a positive for the economy as a whole (creates more consumer spending or allows debtors to pay down personal liabilities like credit cards). A falling trend of purchase applications indicates a decline in home buying demand, a negative for the housing industry and the economy as a whole.</p

Excerpts from the Release…</p

The Market Composite Index, a measure of mortgage loan application volume, increased 13.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 12.4 percent compared with the previous week. The four week moving average for the seasonally adjusted Market Index is up 2.6 percent.</p

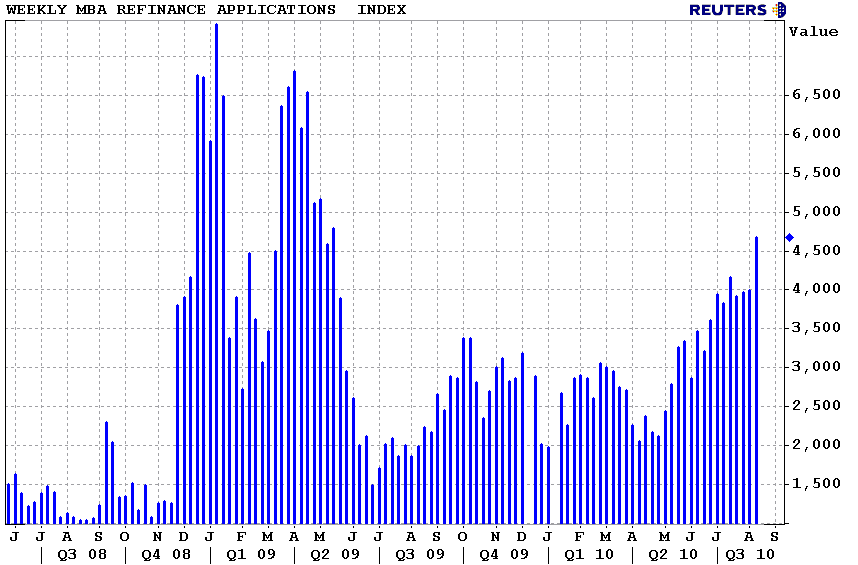

The Refinance Index increased 17.1 percent from the previous week and was the highest Refinance Index observed in the survey since the week ending May 15, 2009. The four week moving average is up 3.2 percent for the Refinance Index. The refinance share of mortgage activity increased to 81.4 percent of total applications from 78.1 percent the previous week, which is the highest refinance share observed since January 2009.</p

</p

</p

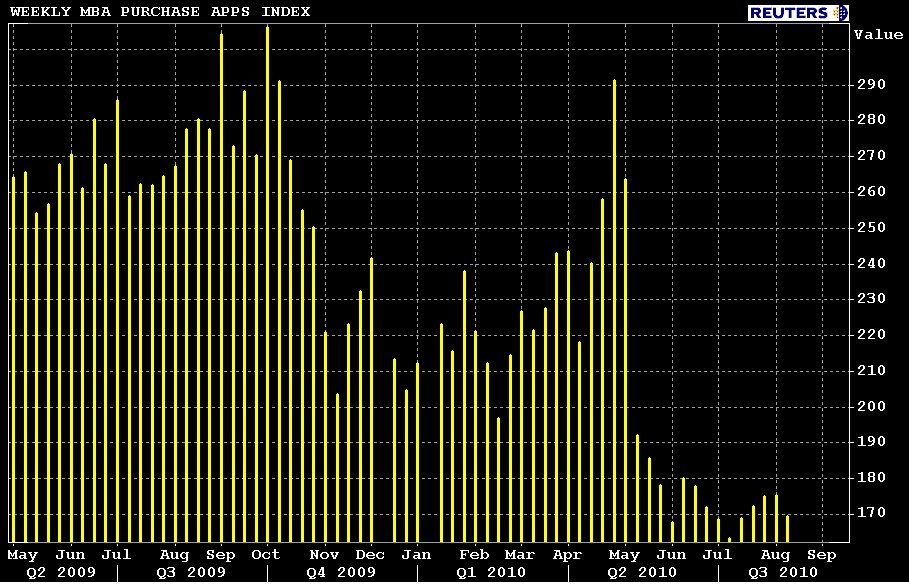

The seasonally adjusted Purchase Index decreased 3.4 percent from one week earlier. The unadjusted Purchase Index decreased 4.6 percent compared with the previous week and was 38.6 percent lower than the same week one year ago. The four week moving average is up 0.1 percent for the seasonally adjusted Purchase Index.</p

</p

</p

Just in case you forgot (haha amusing), here is a reminder of where purchase apps stand in terms of the big picture. Looks a lot like a Housing Starts or Building Permits chart doesn't it? Have purchase apps found a bottom yet??? VOTE HERE</p

</p

</p

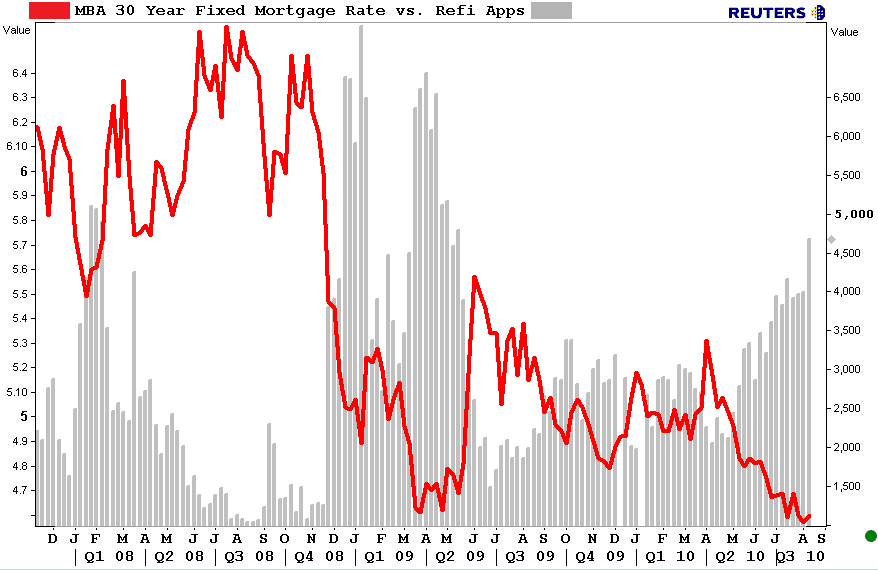

The average contract interest rate for 30-year fixed-rate mortgages increased to 4.60 percent from 4.57 percent, with points increasing to 0.92 from 0.89 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. The effective rate also increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 3.99 percent from 3.95 percent, with points decreasing to 1.05 from 1.08 (including the origination fee) for 80 percent LTV loans. The effective rate also increased from last week.

The average contract interest rate for one-year ARMs decreased to 6.90 percent from 7.00 percent, with points decreasing to 0.21 from 0.22 (including the origination fee) for 80 percent LTV loans. The adjustable-rate mortgage (ARM) share of activity decreased to 5.7 percent from 5.9 percent of total applications from the previous week.</p

</p

</p

Interesting…the MBA says mortgage rates actually rose last week. I have to disagree with that, mortgage rates did improve last week, but I understand why the MBA survey might be indicating mortgage rates rose: because they survey RETAIL lenders </p

Because mortgage rates are at all-time lows, more and more consumers (not as many as last year) are coming down off their fences and applying for a refinance. This week the Refinance Index hit its highest mark since the week ending May 15, 2009. Refinance demand is driving activity in the mortgage market and lenders are operating near full-capacity. When this happens, lenders generally let loan pricing worsen to control the pace of new loan production and protect their pipeline from fallout risk. This is playing out right now in the primary mortgage market AT THE LARGE RETAIL LENDERS SPECIFICALLY. Besides potentially higher borrowing costs, consumers and loan officers should also notice longer “turn times” at lenders, which is basically the amount of time it takes to go from application to closing.

Have you noticed longer “turn times” lately?</p

READ MORE: PRIMARY/SECONDARY SPREADS WIDENED AFTER AN INFLUX OF LOCKS LAST WEEK</p

I have a question for loan originators…</p

How many of these new refinance applications are borrowers who have refinanced within the last 20 months? Are you getting more refinance inquiries from borrowers who are currently paying interest only?

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment