Blog

LPS: Delinquency Measures Improve but Timelines Grow

The latest Mortgage Monitor report from Lender ProcessingrnServices (LPS) shows a housing market where things are improving slowly, while partsrnof the infrastructure appear to be slipping into dysfunction, especially inrnthose states that utilize a judicial process of foreclosure. </p

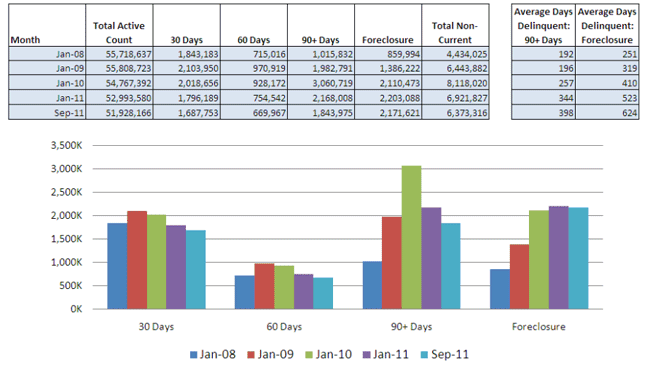

The underlying problems do seem to be easing. Delinquencies dropped one-half of one percentrnfrom August to September to a national rate of 8.09 percent, 12.7 percent belowrnthe rate in September 2010. On the otherrnhand, newly delinquent loans (loans that had been current 60 days earlier) havernincreased steadily since June and now represent 1.6 percent of all loans. Still this is only about half the number ofrnnew delinquencies entering the system in late 2008 through early 2010. . It isrndisquieting to note that the states that have had the most persistent highrnlevels of foreclosures – Nevada, Arizona, Florida – are still running well abovernthe national average, with new delinquencies in Nevada now at 3.21 percent. About a quarter of early-stage delinquencies havernin arrears for the first time, a figure that has been relatively consistentrnsince the beginning of the year. </p

At the end of the reporting period there were 6.4 millionrnnon-current loans nationwide, down from 6.9 million in January. Of these, just over 4.1 million are seriouslyrndelinquent (over 90 days) or in foreclosure compared to 4.4 million at thernbeginning of the year. </p

There were a total of 22,273 foreclosure starts during thernmonth, 11.2 percent fewer than in August and 20 percent less than one yearrnearlier. Loans in foreclosure representrn4.18 percent of all loans in the country, up 1.7 percent from July and nearly 9rnpercent from one year ago. </p

</p

</p

Despite the shrinking numbers throughout the system, the processrnis stagnating in places and delinquency is becoming chronic. Loans are not being processed out of thernsystem either through foreclosure or cure. rnIn January 2008 a seriously delinquent loan had been delinquent for anrnaverage of 192 days, today that average is 398 days, up from 344 just sincernJanuary. In January 2008 it took 251rndays for a loan to wend its way from first delinquency to foreclosure; todayrnthat average is 624 days, up 101 days just since the first of this year. Almost 40 percent of loans in foreclosure havernnot made a payment in two years and 72 percent have not made a payment in atrnleast a year. </p

</p

</p

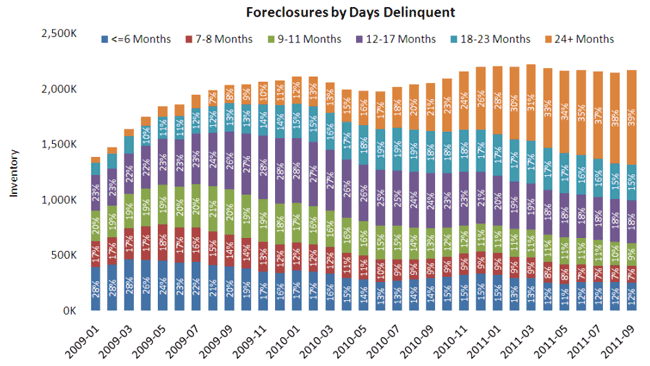

The situation is even worse in the 24 states that rely fullyrnor primarily on a judicial form of foreclosure. rnSeven of the top 10 states by percentage of non-current loans are judicialrnand the foreclosure inventories in these seven states now account for nearlyrnseven percent of the entire active loan count. rnAnd not only are delinquencies growing in those states, but so is therntimeline for those foreclosures. Therntime from last payment to foreclosure sale in judicial states is now 761 days,rnsix months longer than in non-judicial states and only 1.6 percent of thernforeclosure inventories in those states are moving to sale compared to 7.3rnpercent in non-judicial states. Foreclosure inventories as a percent of loansrnin non-judicial states at the beginning of 2008 were 1 percent and 2 percent inrnjudicial states. Today the inventoriesrnstand at around 2 percent in non-judicial states and over 6 percent in judicialrnstates. </p

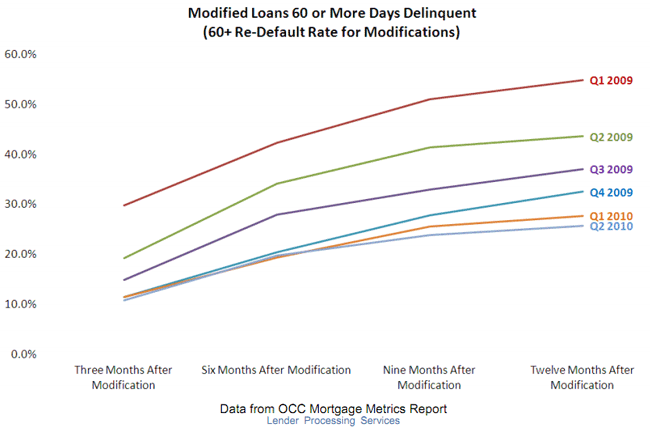

Loans are also not being positively resolved in the volumes theyrnwere earlier. Modifications fell from 160,000 in March to 149,000rnin June with a big drop proprietary modifications more than offsetting a risernin HAMP conversions. There has been arndecided improvement in the success of those modifications, however, with therndefault rate after 1 year running around 20 percent for loans modified in 2010rncompared to 50 percent for earlier modifications at the same age.</p

</p

</p

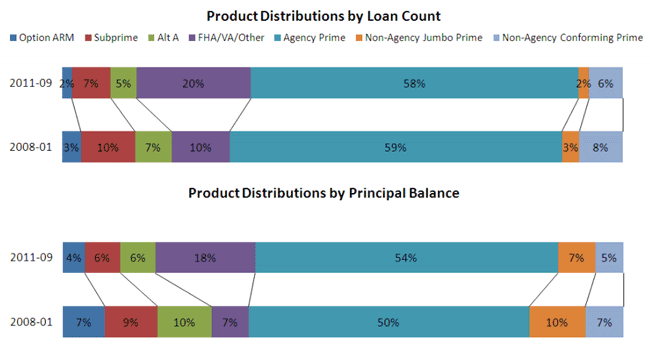

The LPS report notes that the government share of thernmortgage market has increased markedly since the beginning of the mortgagerncrisis, with most of that uptick both in numbers of loans and outstandingrnmortgage balances coming in the FHA/VA markets as those loans appear to have pickedrnup the slack as Option, Alt-A, and subprime loans declined.</p

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment