Blog

OCC Notes Fewer Banks Tightening Underwriting Standards

The Office of Comptroller of the Currencyrn(OCC) recently completed its 18th annual “Survey of CreditrnUnderwriting Practices.” The survey seeks to identify trends in lendingrnstandards and credit risks for the most common types of commercial and retailrncredit offered by National Banks and Federal Savings Associations (FSA). The latter was included for the first time inrnthis year’s survey.</p

The survey covers OCC’s examinerrnassessments of underwriting standards at 87 banks with assets of three billionrndollars or more. Examiners looked atrnloan products for each company where loan volume was 2% or more of itsrncommitted loan portfolio. The survey coversrnloans totaling $4.6 trillion as of December 31, 2011, representing 91% of totalrnloans in the national banking and FSA systems at that time. The large banks discussed in the report arernthe 18 largest by asset size supervised by the OCC’s large bank supervisionrndepartment; the other 69 banks are supervised by OCC’s medium size andrncommunity bank supervision department. rnUnderwriting standards refer to the terms and conditions under whichrnbanks extend or renew credit such as financial and collateral requirements,rnrepayment programs, maturities, pricings, and covenants.</p

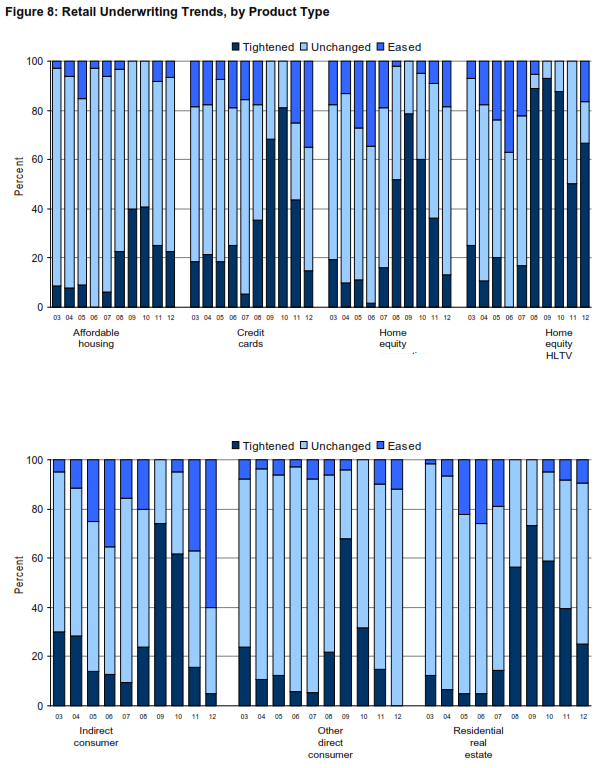

The results showed that underwritingrnstandards remain largely unchanged from last year. OCC examiners reported that those banks that changedrnstandards generally did so in response to shifts in economic outlook, therncompetitive environment, or the banks risk appetite including a desire forrngrowth. Loan portfolios that experiencedrnthe most easing included indirect consumer, credit cards, large corporate,rnasset base lending, and leverage loans. rnPortfolios that experienced the most tightening included highrnloan-to-value (HLTV) home equity, international, commercial and residentialrnconstruction, affordable housing, and residential real estate loans.</p

Expectations regarding future health ofrnthe economy differed by bank and loan products but examiners reported thatrneconomic outlook was one of the main reasons given for easing or tighteningrnstandards. Others were changes in riskrnappetite and product performance. Factors contributing to eased standards were changesrnin the competitive environment, increased competition and desire for growth andrnincreased market liquidity. </p

The survey indicates that 77% ofrnexaminer responses reflected that the overall level of credit risk will remainrneither unchanged or improve over the next 12 months. In last year’s survey 64% of the responsesrnshowed an expectation for improvement in the level of credit risk over therncoming year. Because of the significant volume of real estate related loans,rnthe greatest credit risk in banks was general economic weakness and its resultsrnand impact on real estate values. </p

Eighty-four of the surveyed banks (97rnpercent) originate residential real estate loans. There is a slow continued trend fromrntightening to unchanged standards with 65 percent of the banks reportingrnunchanged residential real estate underwriting standards. Despite the many challenges and uncertaintiesrnpresented by the housing market, none of the banks exited the residential realrnestate business during the past year however examiners reported that two banksrnplan to do so in the coming year. Additionally,rnexaminers indicated that quantity of risk inherent in these portfolios remainedrnunchanged or decreased at 81% of the banks.</p

Similar results were noted forrnconventional home equity loans with 68% of banks keeping underwriting standardsrnunchanged and 18% easing standards since the 2001 survey. Of the six banks that originated highrnloan-to-value home equity loans, three banks have exited the business and onernplans to do so in the coming year</p

</p

</p

Commercial real estate (CRE) productsrninclude residential construction, commercial construction, and all other CRErnloans. Almost all surveyed banks offeredrnat least one type of CRE product and these remain a primary concern of examinersrngiven the current economic environment and some banks’ significantrnconcentrations in this product relative to their capital. A majority of banks underwriting standardsrnremain unchanged for CRE; tightening continued in residential construction andrncommercial (21 percent and 20 percent respectively). Examiners site cited the distressed realrnestate market, poor product performance, reduced risk appetite and changingrnmarket strategy as the main reasons for the banks net tightening.</p

Nineteen banks (22 percent) offeredrnresidential construction loan products but recent performance of these loansrnhas been poor and many banks have either exited the product or significantlyrncurtailed new originations.</p

</p

</p

Of the loan products surveyed 17% were originatedrnto sell, mostly large corporate loans, leveraged loans, international credits,rnand asset based loans. Examiners notedrndifferent standards for loans originated to hold vs. loans originated to sellrnin only one or two of the banks offering each product. There has been continued improvement sincern2008 in reducing the differences in hold vs. sell underwriting standards andrnOCC continues to monitor and assess any differences.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment