Blog

Servicers Report Loan Performance Continued to Increase in Q4

The Office of Comptroller of the Currency (OCC) is reporting that the quality of mortgage loans serviced by selected national and federal savings banks continued to improve in the fourth quarter of 2012. OCC’s Mortgage Metric Report covers 29.0 million loans with $4.9 trillion in principal balances, approximately 57 percent of outstanding mortgage loans in the U.S.</p

Current and performing loans increased from 88.6 percent in the third quarter to 89.4 percent at the end of December. In December 2012 performing loans constituted 88.0 percent of first lien mortgages. The 30+ day delinquency rate was 2.9 percent, a decline of 8.2 percent from the third quarter and 6.1 percent from a year earlier. Serious delinquencies – over 60 days or held by borrowers in bankruptcy, represented 4.4 percent of loans, unchanged from both the second and third quarters but down 11.6 percent from Q4 2011.</p

</p

</p

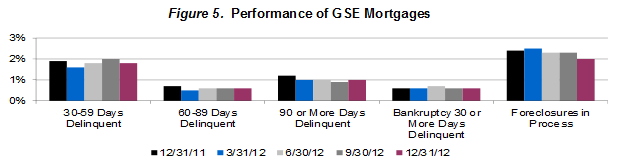

Mortgages serviced for Freddie Mac and Fannie Mae (the GSEs) made up 57.9 percent of those in the report and had a 94 percent current and performing rate. The 30+ day delinquency rate was 1.8 percent, down from 2.0 and 1.9 percent in the previous quarter and one year earlier.</p

</p

</p

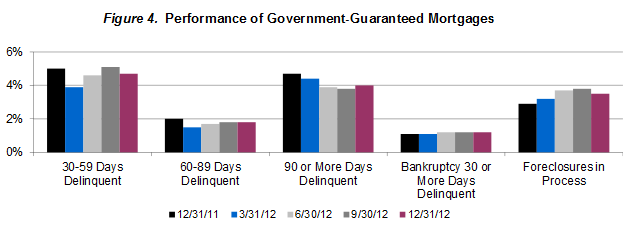

Government guaranteed mortgages made up 23.7 percent of the serviced portfolio and 84.7 percent of those loans were current and performing. The serious delinquency rate (90+ days) of these mortgages increased from 3.8 percent in the third quarter to 4.0 but this was still lower than the 4.7 percent rate one year earlier.</p

</p

</p

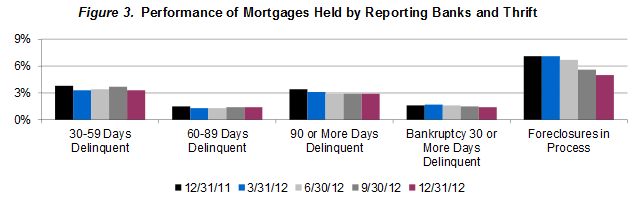

The nine institutions reporting to OCC held 8.3 percent of the mortgages covered in the report in their own portfolios. At the end of the quarter 85.9 percent were current and performing, up from 82.6 in Q3. The 30+ day delinquency rate was 3.3 percent, a decrease of 9.3 percent from Q3 and 12.1 percent in Q4 2011. Five percent of these mortgages were in foreclosure, 10.7 percent fewer than the previous quarter and 29.4 percent less than one year earlier.</p

</p

</p

Since the first quarter of 2009, mortgages held in the servicers’ portfolios have performed worse than mortgages serviced for the GSEs because of concentrations in nontraditional loans and weaker geographic markets and, more recently, delinquent loans repurchased from investors.

The number of loans in the process of foreclosure at the end of 2012 fell below one million for the first time since the end of June 2009. In the fourth quarter of 2012, servicers initiated 156,773 new foreclosures-the lowest number of new foreclosures since the OCC began tracking them in the first quarter of 2008. The number of completed foreclosures fell to 105,875, a 7.7 percent decrease from the previous quarter and an 8.9 percent decrease from a year earlier. Short sales decreased 3.3 percent from the previous quarter and 2.4 percent from a year earlier and constituted 36.5 percent of total home forfeiture actions, up from 35.4 percent the prior quarter. Deed-in-lieu-of-foreclosure actions remained a small portion of home forfeiture actions during the quarter.</p

Several factors contribute to the year-over-year improvement in delinquencies and foreclosures including strengthening economic conditions, the ongoing effects of both home retention and home forfeiture actions, and servicing transfers to institutions outside the federal banking system.</p

</p

</p

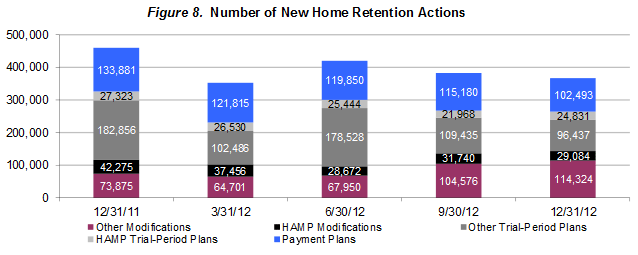

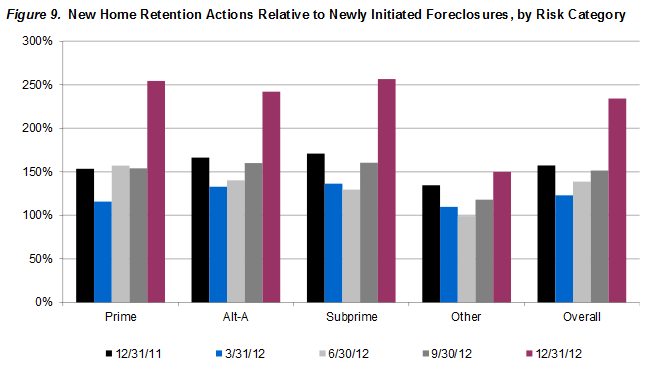

Servicers continued to emphasize alternatives to foreclosure during the quarter, implementing 367,169 home retention actions compared with 169,064 home forfeiture actions. These included 143,408 modifications, 121,268 trial period plans, and 102,493 payment plans. HAMP modifications decreased 8.4 percent from the previous quarter to 29,084 and are down 31.2 percent form the fourth quarter of 2011 while other modifications increased 9.3 percent quarter-over-quarter and 54.9 percent year-over-year to 114,324. Overall, the number of home retention actions implemented by servicers decreased by 4.1 percent from the previous quarter and decreased 20.2 percent from the prior year.</p

</p

</p

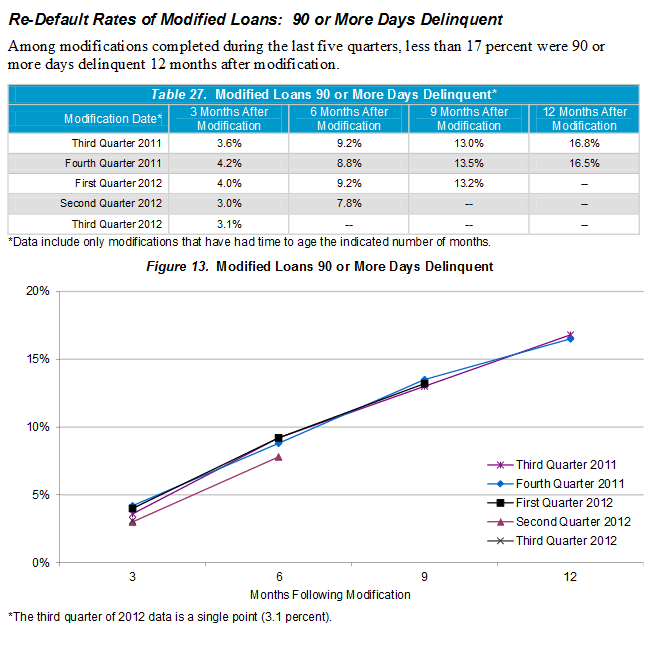

Servicers have modified 2,878,228 mortgages since the beginning of 2008 through the end of the third quarter of 2012. At the end of the fourth quarter of 2012, 47.7 percent of these modifications were current or paid off. Another 7.1 percent were 30 to 59 days delinquent, and 14.2 percent were seriously delinquent. There were 7.7 percent in the process of foreclosure, and 7.3 percent had completed the foreclosure process.

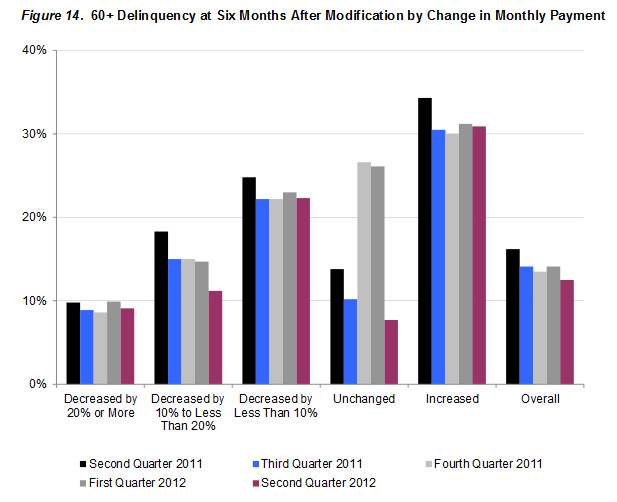

Modifications on mortgages held in the servicers’ own portfolios or serviced for the GSEs have performed better than modifications on mortgages serviced for other investors, perhaps reflecting differences in loan risk characteristics and modification programs, and additional flexibility to modify terms of portfolio mortgages for greater sustainability. Re-default rates for government-guaranteed mortgages and loans serviced for private investors were highest over time, reflecting the higher risk characteristics associated with those mortgages. For all investors, re-default rates have decreased over time as more recent modifications have focused more on reducing monthly payments and increasing borrowers’ ability to sustain the reduced payments over time.</p

</p

</p

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment